The 2013 reporting year is getting into full swing now as annual reports (including a detailed remuneration report) start to be released. Here at Egan Associates we’re enjoying the influx of new data. Unfortunately, we’re also already coming down with the perennial headaches caused by poorly written remuneration reports.

Taking inspiration from the reports of the season, we’ve put together a few remuneration report dos and don’ts.

DON’T:

-

Muddle your maximum and target incentive levels

We’ve mentioned this previously in our February newsletter, but it’s still happening. Target incentive awards are generally provided for on-budget performance, while maximum payouts only occur if both the company and the executive exceeded all expectations. There is no such thing as target maximum. Note – if it is necessary to add or multiply the performance payout for various performance hurdles to achieve an overall maximum, the disclosure is not reader friendly.

-

Withhold information on LTI valuations

Many companies are now providing additional tables stating the value of equity awarded under long term incentive plans that has vested in the year. This is encouraging, but if you’re going to do this, please explain what assumptions you have used to arrive at the LTI values.

-

Gloss over your peer group choice for comparative performance hurdles

The choice of a peer group will be a large influence on whether the LTI incentive will vest, so stakeholders have a right to know what was behind your choice.

-

Put the chicken before the egg

Make sure you plan the flow of information so stakeholders don’t have to flick back and forth through the report to understand. For example, it doesn’t make sense to state what proportion of a short term incentive grant was awarded if we don’t yet understand how the short term incentive works.

-

Insert large blocks of text

Remuneration is difficult enough to comprehend without adding density. You can avoid text overload in a number of ways: using pictures, tables, dot points, adding whitespace, or simply breaking up paragraphs.

-

Add redundant information, or information “just in case”

Because of the increasing length of remuneration reports, each table, each picture and each paragraph needs to be subjected to three questions:

- Is this information necessary for stakeholders to make a judgement on KMP remuneration, or can it be removed?

- If it is necessary, have I provided this information somewhere else?

- If so, can I simply reference the place I have mentioned this information before or does it need to be repeated here?

DO

-

Provide an overview of the sections of the remuneration report at the start of the document

This will help readers find what they want to look at quickly.

-

Summarise remuneration changes since the prior year in one brief section

This will quickly inform stakeholders what has been done to address their concerns. If changes are afoot but not yet implemented, they can also be flagged here.

-

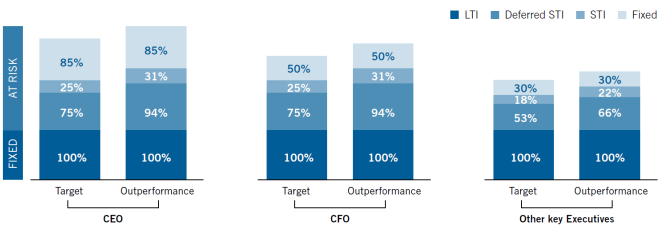

Use a graph to demonstrate the remuneration mix

A paragraph listing percentages is not easy to read, for example this one:

Exec A has a maximum STI reward equivalent to 12 months fixed remuneration of $x and maximum LTI reward equivalent to $y. Accordingly, Exec A’s total maximum remuneration package comprises approximately a% fixed remuneration, approximately b% target ‘at risk’ STI and approximately c% target ‘at risk’ LTI, totalling $z.

Instead, use a graphic to quickly illustrate proportions. For example, this diagram illustrates the remuneration mix at target and maximum for Dexus:

-

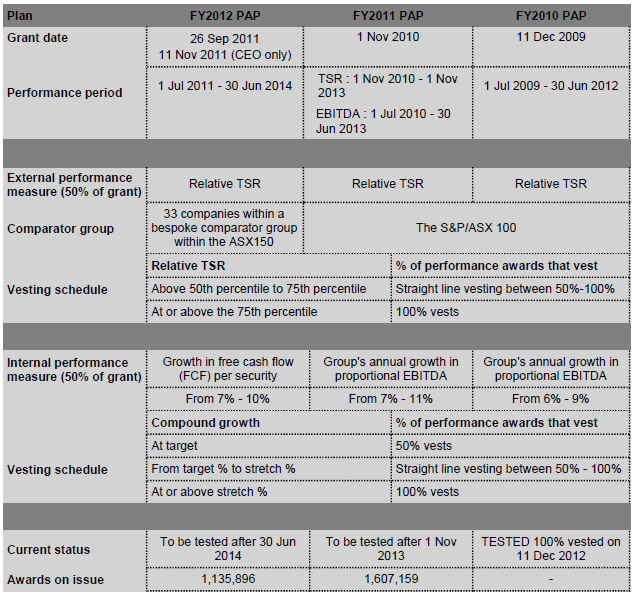

Use tables to describe the features of STI and LTI plans

Doing this helps readers to scan the details quickly. Try and keep the information in the table standard, with new row for each new set of data – performance period, performance hurdle, vesting schedule etc. For example, see this table published by Transurban to summarise its legacy plans:

-

Carefully explain unique incentive plans

If the way your plans function is unique to your organisation, you will need to take extra time to think about how best to explain the details. Consider whether a table or a flowchart will help you present key points.

-

Disclose the methodology used to reach the number of equity instruments granted to executives as incentives

Did you use the market value or a discounted value to calculate the number? If the latter, what kind of discount and why?

-

Use consistent terminology

- Not only should you use the same terms to describe remuneration elements throughout your report, but if possible, you should also use terms that are being used by the rest of the industry. If most companies are using a particular name for a remuneration element, there’s probably a reason.

- Make sure your remuneration abbreviations don’t clash with abbreviations in different sections of the annual report. For example, LTI can’t stand both for long term incentive and lost time to injury. To make things perfectly clear, a glossary and abbreviations listing at the end of the report will help readers keep track. This isn’t an excuse to add as many three letter acronyms as you like though – the report will begin to feel like alphabet soup.

Remuneration Report Evolution

- So far, although we’ve seen many additional tables stating the actual remuneration an executive received in the year, there have been few examples where the company has referenced the draft disclosure legislation and explicitly labelled and segmented remuneration elements as past, present and future remuneration.

- We would note that those adding additional tables should make sure they clearly label the additional table to avoid confusion. It might also be advisable to either place the table of actual remuneration and the statutory table close together or reference the location of the statutory table in the text explaining the actual remuneration table.

- Clawback/malus clauses are becoming commonplace, with organisations including clawback/malus for deferred STI and LTI grants not only for material misstatements of the company’s financials, but also for the case of significant reputational damage.

- An increasing number of Boards are exercising their discretion to vest incentive awards for executives, especially where such awards are not otherwise justified by underlying performance. In the interests of transparency and to reinforce shareholder alignment, we strongly recommend full disclosure of both the availability of such discretion (going forward) and the exercise of discretion (after the event).