Long term incentives (LTIs) are the most complex and least understood element of executive remuneration.

Part of the confusion is that there are multiple ways to consider the value of an LTI – many more than we can discuss in this setting. For this article, we have chosen to describe and compare four simple ways to look at the value of LTIs offered to executives.

- Statutory LTI

The statutory long term incentive value is the LTI value most commonly referenced (and misunderstood) in the media.

It is the value in the statutory remuneration table that all companies must disclose. It is not a representation of how much an executive has been granted or paid during the year, but rather the deemed accounting cost to the company of the executive’s LTI grants.

The value displayed for one financial year will contain the amortisation of multiple years’ LTI grants, discounted for the likelihood that an executive will leave before a grant vests and for the probability of the performance hurdles being achieved.

- Disclosed Maximum LTI

This is the intended maximum value of the long term incentive grant to an executive. It is generally disclosed as part of a company’s remuneration mix, most often depicted as a percentage of fixed annual remuneration. Not all companies disclose this value clearly (some report a notional target value), and the smaller the company, the less likely they will disclose it.

- Latest Grant Value

This is the market value of any grant made in the latest financial year. Egan Associates calculates this value using the closing price at grant date. For options this involves an assumption of share price growth.

- LTI on foot

This is the value of all of the long term incentives that have been granted but have not yet vested to the executive. This value (often annualised) can be useful for companies that do not make annual grants. In such cases, the latest grant value can be “lumpy”, zero one year and large the next.

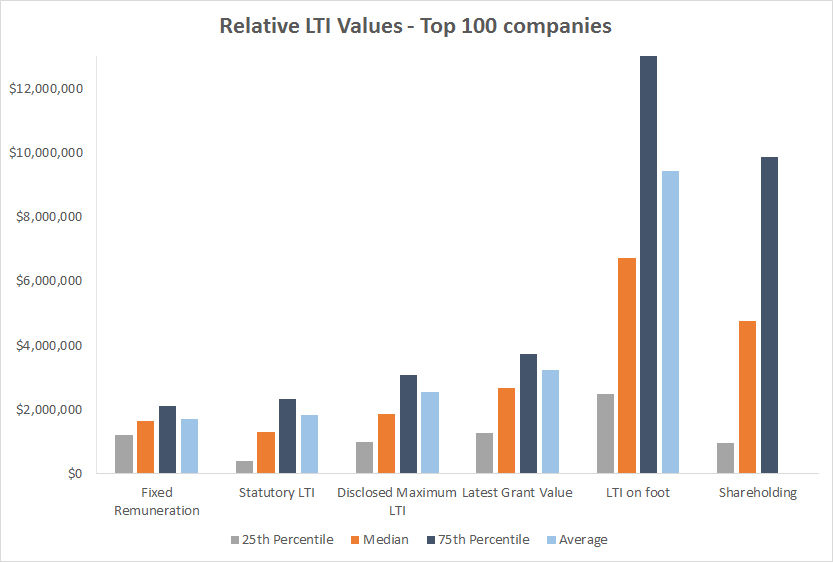

Relative values using these four lenses

To provide an indication of the relative values of each of these perspectives, Egan Associates examined each of these values for the CEOs of top 100 Australian companies.

Since the focus is on relative values, to keep the example simple, we excluded companies with option grants. The results exclude zeros except in the case of the CEO shareholding. The average shareholding value is not shown as it is significantly higher than the 75th percentile due to selected CEOs whose current shareholdings are very large. The value of the LTI on foot (unvested LTI) has been calculated using a smoothed share price from the end of the latest quarter.

Some observations on relativities:

- The statutory LTI is lower than the maximum LTI and the latest grant value because it is discounted for the reasons noted above.

- In an ideal world, the disclosed maximum LTI should equal the latest grant value if this value is calculated at grant date. As can be seen, this is not exactly the case. The median latest grant value is higher than the disclosed maximum LTI. This is partly because some companies are disclosing the value of equity granted to executives based on the fair value of a security at grant date, which will be discounted in comparison to the market price at grant date.

- The LTI on foot value (unvested LTI award value) is significantly larger than the latest grant value, because it comprises the current market value of multiple years of grants. The relative value of the equity on foot demonstrates how valuable LTI can be as a retention mechanism. If the CEO were to leave the company, this is the amount they would forfeit (unless their new employer agrees to a buyout).

- The relative value of the CEOs’ shareholding is lower than the LTI on foot for top 100 companies. Preliminary analysis for smaller companies indicates that the opposite is true. This reflects the more modest levels of LTI (and remuneration in general) for smaller companies and potentially also reflects the likelihood of founding members still being at the helm of those companies.

When benchmarking LTIs, companies may decide to consider one, some or all of the above values, or even additional measures not mentioned here. The decision will depend on the company’s attributes and circumstances. It will also depend on the information available, as when examining international competitors, the same depth of information is often not readily available.

It is important to understand the basis of their disclosures and to make an informed decision about which data is appropriate. Egan Associates assist our clients with these deliberations.