This AGM season Boards will be looking to ensure that short term incentive plans are consistent with Institutional Investor and Proxy Advisor expectations of pay for performance.

There are a variety of ways to measure performance, and these can vary considerably between industries as well as between companies. However Institutional Investors and Proxy Advisors prefer a strong link between pay and shareholder return, and are increasingly critical of payments that are out of line with the company’s performance trend.

Egan Associates has explored the short term incentive payments for CEOs in the ASX 100 relative to companies’ operating profit improvement for the years 2013 and 2014. The companies were ranked by market capitalisation as of 30 September 2015.

The following figure reveals the proportion of companies that recorded an improvement in operating profit over the two-year period.

Figure 1. Proportion of Companies achieving Operating Profit Improvement within the ASX 100

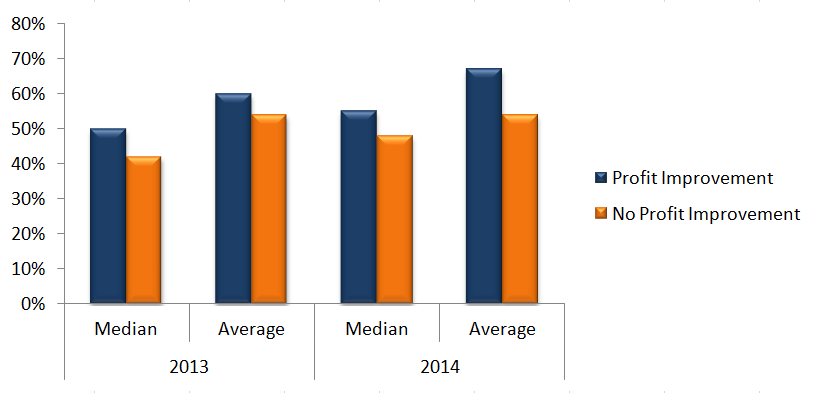

Figure 2 shows the median and average STI payments as a percentage of fixed remuneration, and Figure 3 shows the increase in these payments from 2013 to 2014.

Figure 2. Ratio of STI Awards to Fixed Remuneration within the ASX 100

From 2013 to 2014 the value of STI awards as a ratio of fixed remuneration increased overall, with the median increase in companies with profit improvement (5%) being similar to that in companies where there had been no profit improvement (6%).

In both 2013 and 2014, CEOs leading companies that did not improve their operating profit received an average bonus/incentive payment of 54% of their fixed remuneration. Those in companies that did deliver a profit improvement received an average bonus of 67% in 2014, an increase of 7% from the previous year.

Figure 3. Change in STI Award 2013 to 2014 as a Percentage of Fixed Remuneration

In terms of the median change, there was no significant increase in the value of incentive awards (1%) for companies that did not record an operating profit improvement in 2014, while there was a 14% increase in incentive payments for companies that did.

Also worth noting is the higher proportion of companies with no profit improvement, as opposed to those with profit improvement, where there was a negative change in the value of an award relative to fixed remuneration.

Figure 4. Proportion of Companies where the CEO Received an STI Award

Egan Associates observed that the proportion of companies in the ASX 100 that paid an STI has increased by 11% between 2013 and 2014. An additional 9% of companies paid an STI despite not seeing a profit improvement for the year, which is 7% higher than the observed increase for companies that did record a profit improvement.

{kind=link}

Conclusions

Despite an increase in the number of CEOs receiving incentive payments where the company’s operating profits had not increased, we can observe a positive trend between pay and company performance when the value of awards relative to fixed remuneration is considered.

Egan Associates notes that there are also instances where payments that appear not to reflect a company’s profit performance are nevertheless in line with shareholder expectations. In particular, higher incentive payments can reflect exceptional performance achieved in prior years where there is a lag in disclosure. In addition, payments may be considered well earned, for example, in times of adversity or during corporate restructures.