With a long campaign still to come, it seems clear already that superannuation will feature as a key issue in this year’s election.

Although media focus on superannuation has been intensifying in the last month, the issue of additional taxation on the scheme actually arose in September 2012.

The Australian Financial Review reported that the government wanted to limit the cost of the scheme, which Treasury had identified as the “taxation minimisation vehicle of choice”, with capital gains tax breaks for self-managed superannuation funds the most likely target.

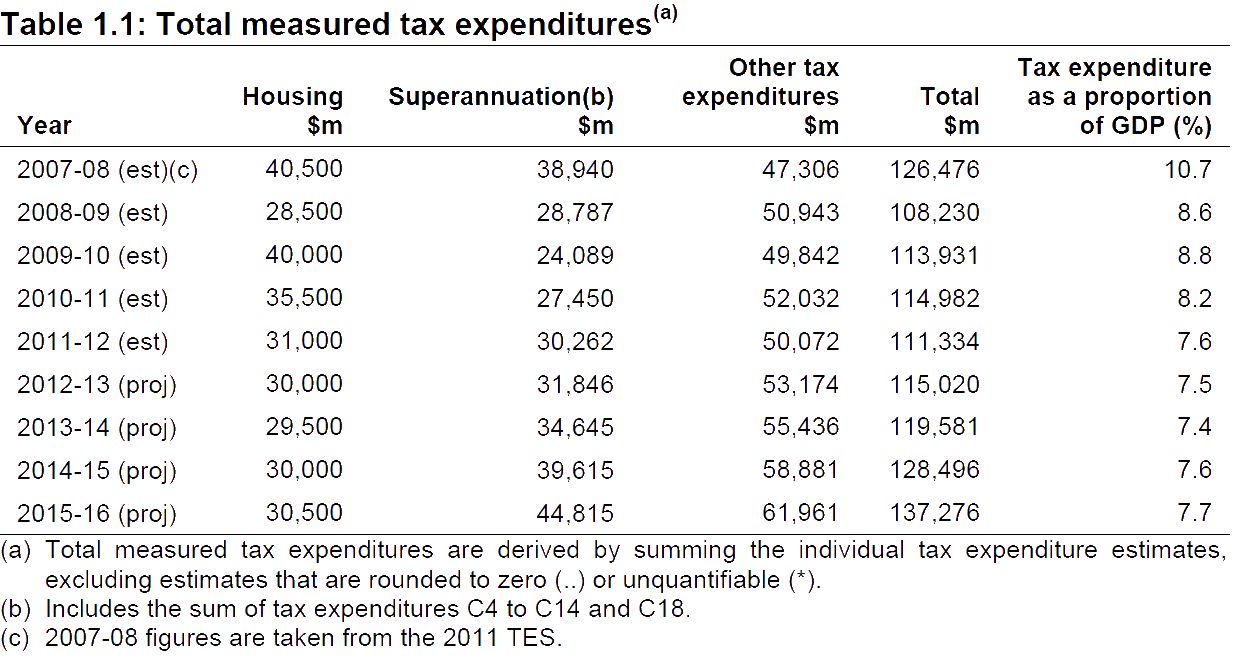

Latest Treasury estimates put the cost of superannuation concessions at almost $32 billion for the 2012-2013 year and projected this to rise to $45 billion in the 2015-2016 year, as recorded in the table below (Tax Expenditure Statement, Australian Government, CC3.0).

Superannuation industry sources had been canvassed in September on how the government could save billions on the scheme and were told “nothing” was off the table, according to The Australian. The industry reacted negatively and the Government decided to canvas further opinions on the matter instead of releasing a policy in the Mid-Year Economic and Financial Outlook.

The Government did not waste time. January saw reports it was considering ending the tax-free status on superannuation withdrawals for funds with balances over $1 million. Treasury analysis had reportedly revealed that in 2009-2010 the top 5% of the nation’s taxpayers received over 20% of the tax breaks for superannuation benefits. The top 10% received 38.2% of superannuation contributions and earnings tax concessions. The Government’s rhetoric was that it was ready to make tough decisions to benefit the true blue Aussie battlers, thereby drawing the battle lines for the campaign to come.

The response from the superannuation industry was alarm at the low threshold for the tax, which would affect a very large number of self managed super funds and many ordinary income earners whose hard-saved nest egg was over the proposed limit. The Opposition followed with its own superannuation concession reduction policy – the abolishment of the Low Income Superannuation Contribution Scheme where workers on incomes below $37,000 are refunded the 15% contributions tax they pay on concessional contributions.

The Government quickly distanced itself from taxing withdrawals, saying it would not tax superannuation withdrawals for those over 60. However, the problem of the high cost of superannuation tax concessions still remained and the Government’s statement leaves open other avenues of taxation.

The Government could turn to a number of options:

- Increasing superannuation earnings tax above 15%.

- Decreasing the threshold beyond which tax payers have to pay a 30% tax on superannuation contributions. (Likely to be lowered from $300,000 to $180,000).

- Abolish the low income earner co-contribution scheme and low income superannuation tax offset.

- Raise the age at which people are able to access tax-free withdrawals for superannuation

The Henry Tax Review had recommended that contributions be taxed at the marginal rate minus a flat rate offset, while the tax on superannuation earnings should be reduced to 7.5%.

The Coalition, meanwhile, has promised to make no further “negative unexpected changes” to superannuation. This is a key point of differentiation, although the wording leaves room for the party to change its mind.

The superannuation industry is understandably concerned about further changes to superannuation, after battling through the Government’s MySuper reforms. The Financial Services Council stated that contributions were down since the GFC, adding that superannuation taxation changes had already had a negative effect. Its research reveals that despite the planned increase to the superannuation guarantee to 12%, there will still be a $836 billion retirement savings gap, $1.227 billion if those Australians who live longer than average are taken into account. It states that every 1% increase in discretionary contributions shrinks the retirement savings gap by $77 billion.

It’s also worth noting that a recent Mercer study calculated retirement tax concessions in nine countries, including the rates of tax on contributions, investment income and retirement income, and found that the UK Kingdom, the United States, Canada and the Netherlands had more generous systems than Australia.

The Australian superannuation industry believes the secret to the system working is stability, which enables those contributing to believe putting their money into super is a safe investment.

However, as we wrote in our November newsletter, some would argue the system is already broken. CPA Australia released a report outlining disappointing superannuation savings for the average Australian and noting a trend towards increased debt in the final years before retirement. In the foreword to the report, CPA chief executive Alex Malley warned that Australians were treating superannuation as a windfall to pay off their mortgage or take an expensive overseas holiday and then when the money was gone, falling back on the old age pension. This means effectively that the government pays twice for people’s retirement. This would suggest that the government both needs to reconsider allowing tax free lump sum superannuation payments, foreshadowed after the report’s release by Superannuation Minister Bill Shorten, and consider whether its current concessions are achieving its superannuation policy objectives.

Although stability is key to Australia’s confidence in the Superannuation Scheme, it is not helpful to continue concessions that are inefficient or do not achieve the scheme’s policy objective. It may be necessary to further reform the superannuation system if it is not functioning in the way it was intended. However, if further changes are made, they should not be for short term gains, but rather steps in a longer-view reform process.