Egan Associates has followed with great interest the activity of the Corporations and Markets Advisory Committee (CAMAC) as it proposed reforms to improve remuneration disclosure requirements. With the release of the draft Corporations Legislation Amendment (Remuneration Disclosures and Other Measures) Bill 2012 supporting implementation of many of CAMAC’s recommendations in mid-December, we felt it timely to offer a perspective.

The legislation changes are:

|

Remuneration Report Disclosure Additions |

Remuneration Report Disclosure Reductions |

|

|

We agree with the disclosure of clawback information and termination related payments. Many companies are already reporting this information.

The more complex proposal to describe remuneration in terms of “past, present, and future” is a well intended attempt to guard against arrangements that obscure real remuneration. The proposal does not, however, meet many shareholders’ need for information about what pay was “earned” during the year. This would embrace fixed remuneration including salary and benefits received, the annual incentive approved in relation to the year under review and the value of long term equity awards which vested having met performance hurdles during the year. This is an area we believe needs consideration.

|

Past pay has been defined by the draft legislation as the “total amount of remuneration that was granted to the person before the start of the year and paid to the person during the year”. (LTI and STI security grants that vest during this year and STI cash amounts for performance in the previous year but paid in the reporting year.) Present pay is the “total amount of remuneration that was granted, and paid, to the person during the year”. (Fixed remuneration and any STI cash or shares granted and vested in the same year.) Future pay is the “total amount of remuneration that was granted to the person during the year (whether or not payment is dependent on satisfaction of a performance condition), but that is not to be paid to the person until after the end of the year”. (STI and LTI security grants made this year but are yet to vest.) |

In terms of the complexity of the proposal, many commentators were disappointed at the lack of a reduction of existing requirements in the draft legislation and warned that organisations will have to include three additional tables to house the information required by the legislation. Yet a large number of companies will already be complying with the requirements without adding additional tables, as they have adjusted to the recommendations released by CAMAC in 2011.

These organisations would not have to add new elements to comply with the draft legislation, except for perhaps summing figures to provide the “total amount” of remuneration for past, present and future pay (with documentation explaining which figures have been summed for each element).

Past pay is often now already being captured by the crystallised LTI and STI payments set out in the tables outlining executives’ take home pay for the year, as is present pay. Future pay is often recorded in a table of grants made to executives in the year, sometimes as separate tables for STI and LTI equity. For example, on page 63 of Westpac’s 2012 Annual Report, the past pay and present pay is set out in a table of remuneration outcomes. The future value of 2012 grants (LTI and STI) are laid out in a table on page 69.

There are two issues that would need to be resolved in this case:

- Westpac, along with many other companies, currently note the STI to be paid for the 2012 financial year’s performance in its annual report as this year’s STI pay, although the executive will not generally be paid this amount until after the completion of the financial year. Under the draft legislation, the STI payment for 2011 performance would technically be noted as past pay. The STI earned with the current year’s performance would be noted as future pay.

- To value performance rights, Westpac has used the equity’s fair value, discounting for expected dividend yield and chance that LTI hurdles will not be met. It is not clear from the draft legislation whether the amount of remuneration granted in the year should be disclosed at face value or accounting value. We believe companies should provide the face value of shares or rights at grant date to provide shareholders with information on remuneration intent and opportunity at market at the time of grant. Options could be priced at the market rate at grant date or using an accounting method that does not take into consideration the uncertainty of meeting performance hurdles.

Other points to note:

- To determine the total amount of past pay, present pay and future pay, organisations will need to be certain of when remuneration is “paid” to an executive. Egan Associates takes paid as meaning the executive has received the remuneration. For equity grants, if shares vest to an executive due to a performance condition being met, we would consider the executive to have received that reward. If vesting involves a service condition, benefit does not arise until the tenure period has been served. In the case of option grants, the payment is not actually “received” by the executive until the executive exercises the options, otherwise the value to the executive is not known.

- As mentioned above, perhaps a more meaningful disclosure for shareholders is pay earned during the year, although this measure does not reveal the monies actually received during the year, which is the subject of the reporting period.

Although we believe the draft legislation’s requirements need not add excessive complexity, there are organisations not disclosing the same amount of information as highly ranked companies such as Westpac. If these organisations decide to “tick the boxes” in conformity with the legislation, it is possible we will see the misguided addition of new tables in the remuneration report, each with its own explanatory notes. This will only add to its length and cause confusion as shareholders attempt to make sense of the detail.

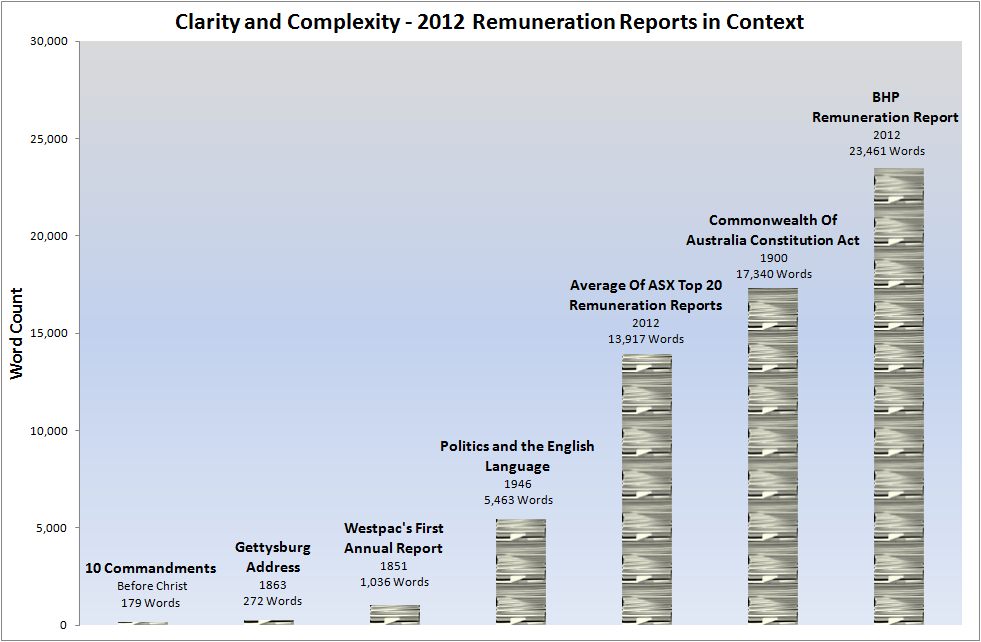

Much has been made of the length of current disclosures and a simple argument can be made that, at an average of nearly 14,000 words, the typical remuneration disclosure now far exceeds that of some other notable texts which arguably carry greater explanatory power.

Click to enlarge

Many would urge, given this context, for no more complexity to be added to remuneration reports. However brevity does not automatically bring clarity.

|

“Everything should be made as simple as possible, but no simpler.” – Albert Einstein. |

Dexus, which received a strike in the 2011 AGM season, illustrated this point well. After the strike, it introduced new short term and long term incentive plans. This meant increasing the length of its remuneration report by a third to ensure the plans were properly communicated. In 2011, only 28.2% of those voting on the remuneration report approved it. In 2012 it achieved 98.3% approval. JPMorgan singled Dexus out as having made the most positive changes to remuneration of those in the top 100 who had received a strike in 2011.

With so many stakeholders taking a perspective on the issue of remuneration, extensive disclosures may be unavoidable. So long as executive talent remains an element of competitive advantage, companies will strive to outmanoeuvre each other both in the quantum and creative structure of the remuneration they offer. In our view, shareholders are well served by this competition so long as it leads to plans that emphasise alignment of executive pay with the creation of shareholder value

The important thing, in our view, is for organisations to follow the spirit of the legislation, rather than copying and pasting paragraphs and tables to fulfil each requirement separately. In this way, we will achieve better engagement between Boards and shareholders.

This may require changes to the draft legislation itself to reveal how the new requirements fit into current requirements, a best practice guideline to accompany future legislation, or clarification in another form on how organisations should relay the necessary information in a brief, clear and transparent manner. The focus should be on achieving clarity without sacrificing transparency.

|

Through the recent AGM season, Egan Associates has been heartened by the willingness of shareholders to vote favourably on remuneration strategies that we have helped our clients to develop and explain. In instances where strikes, or threats of strikes against the remuneration report had been recorded in the prior year, it is obvious that a more transparent explanation and appropriate shareholder engagement led to a circumstance which did not require radical change, but clarity in describing the remuneration structure and incentive plans. We thank all of our clients for placing their trust in us in 2012. |