It has been over a year since the Australian Treasury released draft legislation to improve the employee share scheme provisions under the Income Tax Assessment Act.

For the most part the changes, which were passed by Parliament and took effect on 1 July 2015, have been well received, particularly in relation to the more favourable treatment of options (now generally taxed on exercise rather than on grant).

As such, it was expected that options would increase in popularity among companies issuing securities to key employees as part of an incentive plan.

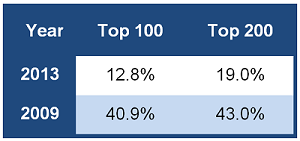

In 2014, Egan Associates examined the top 200 companies by market capitalisation at 31 December 2013 that disclosed LTI grants in their 2013 and 2009 annual reports and determined the proportion that granted options or loan backed share plans (which act like options).

The analysis returned the following results for all executives including the CEO:

Egan Associates has run this analysis again for the top 200 companies at 31 December 2015, with the following result:

It appears that for this sample, the proportion of companies granting options or similar schemes remains approximately the same as it was before the share scheme rules were introduced. In addition, despite the legislation making it unnecessary to use a loan backed share plan to secure favourable tax treatment for an option like instrument, there are still a number in use. The 2015 result purely considering options is as below:

However, companies may not wish to change a plan that is in place if it is currently working as envisioned, and the ASX top 100 companies were not the intended target of the employee share scheme legislation, but rather the small cap companies and start-ups where there is a significant chance for share price growth to deliver considerable upside to employees.

To illustrate the relative prevalence of option use for companies of varying scale, we examined whether or not companies had expensed a value for options grants to the CEO or CFO in their statutory tables. This is not a perfect measure of whether these companies are granting options, as the statutory table does not reflect whether or not a grant has been made in the financial year – it will be the amortisation of a number of years of grants, and may be zero. However, it does provide an indication for the purposes of comparison between company groups of different scale.

The figure below displays the number of companies that recorded an expense for option grants in their statutory table as a proportion of companies that recorded an expense for either option or share/right grants.

The figure reveals that option grants are typically more prevalent in smaller listed companies, which are usually in or entering the growth phase of the business life cycle. In these entities, it is particularly important that the Executive’s incentive opportunity is closely aligned with the company’s growth strategy. Options encourage necessary risk taking and entrepreneurial acumen by providing a higher upside from share price growth than rights, which in turn benefits the company’s shareholders.

It should be noted that as the ASX rank declines, the number expensing any value for equity grants reduces. Only approximately 40% of companies included in the sample that were ranked 500 or lower recorded grants in their statutory table for the CEO or CFO. Where 2015 data was unavailable (some organisations with December year ends have not yet released their remuneration reports), 2014 data was used.

The figures below examine the relationship between sectors.

Companies in the healthcare sector expense the highest proportion of options in total (>50%), reflecting biotechnology and pharmaceutical organisations.

In the ASX 500, expensing CEO and CFO option grants is more common in the energy, metals and mining, industrials and information and communication (ICT) sectors (>30%), and less common in the consumer and financial sectors (<25%).

In companies ranked below the ASX 500, options comprise more than 50% of all expensed grants to both CEOs and CFOs in each of the metals and mining, consumer and energy sectors. The proportion is marginally lower for industrials companies (47% for CEOs and 46% for CFOs) and lowest for financial companies (27% for CEOs and 33% for CFOs).

The low proportion of option grants in the financial sector could either be the result of decisions to limit risky behaviour and/or high dividend yields.