Legislation was passed late last year that mandates the disclosure of remuneration details for superannuation trustees and executive officers from 1 July 2013. The regulations specifying exactly which remuneration elements are to be disclosed on registered superannuation entities’ websites were registered on 28 June.

ASIC has exempted superannuation organisations from the disclosure until 31 October 2013; from then, organisations must be ready to disclose details in respect of the most recently completed financial year, as well as the preceding financial year.

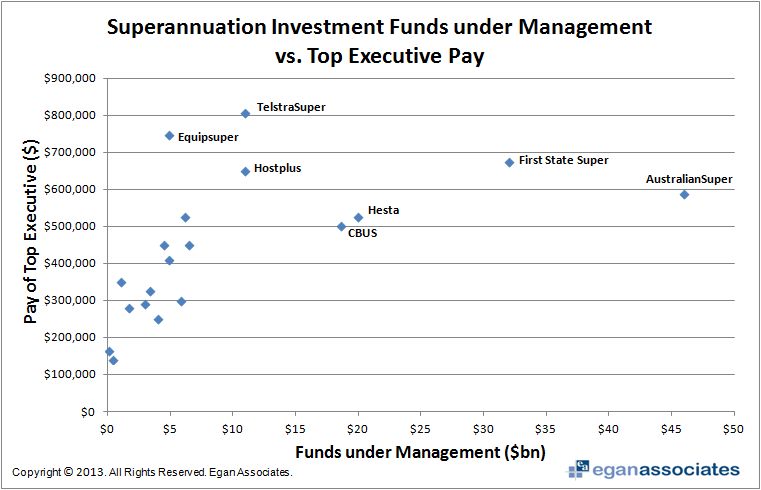

A small number of organisations have already voluntarily begun to disclose information on executive remuneration – working down the APRA list of the largest 200 superannuation funds released in January, we found only 19 that made remuneration information publicly available in their 2011-2012 annual reports. Of those, most disclosed remuneration in bands – the state of remuneration for listed companies between 1987 and 1998.

For those superannuation organisations that disclosed executive remuneration, we found that the top paid executive’s remuneration rises quickly with increasing funds under management. This rise continued to a certain point beyond which the amount of funds under management no longer significantly affected the pay package. The same pattern could be seen for the second highest paid executive.

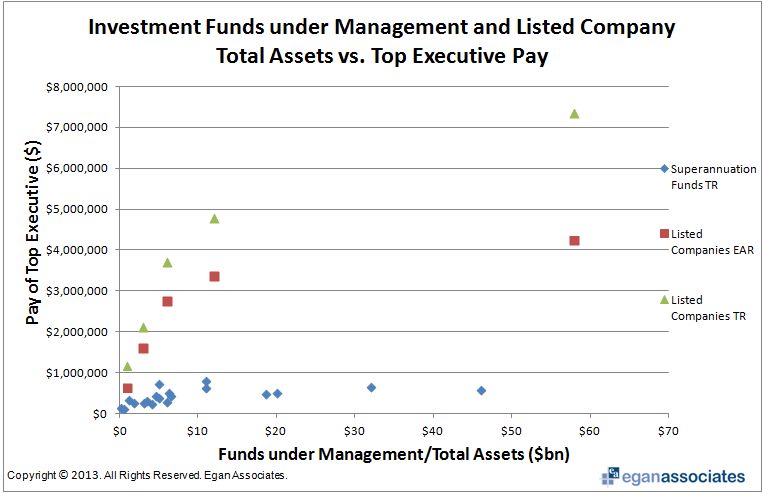

Comparing this remuneration information to the total remuneration (TR) and earned annual remuneration (EAR) of CEOs who manage companies with total assets similar to the superannuation organisations’ funds under management, we found that the superannuation executives were paid relatively much less. In some cases the total remuneration package varied by ten times or more.

The remuneration amounts for the superannuation executives must be interpreted cautiously when compared with CEOs of operating entities. CEOs oversighting a superannuation fund with both administrative and investment accountabilities, whether internally or externally managed, do not have the same accountability as the chief executive of an operating entity. The latter would be accountable for operations, marketing strategy, sales – often across a multitude of jurisdictions – R&D and multiple layers of reporting, including reporting to shareholders.

In addition, trustees and executives often receive remuneration from entities other than the fund itself for work conducted, so the disclosed amounts may not tell the full story of the executive’s remuneration nor reflect actual reward for his or her accountabilities. This is being addressed in the disclosure regulations currently in draft form, which require disclosure of all pay, whether provided by the superannuation organisation or by a related body corporate.

Another issue with the disclosed remuneration is that because pay has generally been disclosed in bands, without information on which executive was awarded which amount, there was often no way to discern whether the executives were remunerated for a whole year or only a portion of the year. There was also often no information as to what the remuneration comprised of – whether it was a fixed or an incentive payment or even a termination payment.

Despite these cautions, the gap between superannuation fund executive remuneration and that of listed companies is large.

There are a number of factors that could have led to this state of affairs.

- The funds under management are not a function of growth, or of the amount of effort required to acquire and manage them, but rather a consequence of the compulsory nature of superannuation.

- The positions examined may be different in that they are of a more analytic and administrative nature rather than investment mandate execution, which is often outsourced.

- We would anticipate that security of tenure would be higher in the superannuation funds management sector than in the highly volatile, extremely demanding and performance reward aligned environment of specialist asset managers or major financial institutions where employment appears to be more elastic and very much focused on the organisation’s performance and capacity to retain mandates.

- Restraint given superannuation entities have been enjoying low levels of return.

- It is possible only those with modest remuneration arrangements voluntarily disclosed remuneration information.

As the next reporting season approaches, it will be interesting to observe whether more organisations report remuneration before they are required to. Since superannuation organisations have been complaining about the lack of disclosure in other companies, they should be ready to set an example and adopt best practice.

Bringing remuneration disclosure into line with that of listed organisations is likely to will be an extremely complicated process for most superannuation organisations, many of which have not disclosed one skerrick of information about executive remuneration. Listed organisations have had years to adjust to the ever increasing disclosure requirements: the first requirements for executive remuneration disclosure became effective in 1987. That’s a quarter of a century worth of change. Superannuation organisations must manage the transition in just one.

1987: Listed companies required to disclose total annual emoluments (cash and non cash remuneration) of executives earning over $100,000 in $10,000 bands. 1998: Introduction of section 300Aa in the Corporation’s Act, requiring disclosure of a remuneration policy and details of pay elements and amounts (including base salary, short and long term incentives and other payments) for Directors and the top five highly paid executives. 2003: ASIC issued guidelines requiring companies to place a reliable valuation on options granted as part of remuneration. Companies could choose Black–Scholes, Lattice (Binomial) or Monte Carlo valuation methods. 2004: Companies required to include remuneration information in a specific remuneration report within the company’s annual report and allow reasonable opportunity for shareholders to make comments on or ask questions about the report, made subject to a non-binding vote. 2007: Disclosure requirements redefined to apply to cover the key management personnel of a company as outlined in accounting standards. New disclosure framework created, transferring accounting standards requirements and Corporations requirements into the Corporations Act and aligning them to remove inconsistencies. 2009: Shareholders required to approve Director and executive termination benefits exceeding a cap of worth over a one year’s base salary. 2011: Two strikes legislation introduced. Companies required to disclose companies the extent to which they received remuneration recommendations advice from and how much that advice those recommendations cost. 2012/2013: Legislation is proposed to also require listed companies to disclose past, present and future pay, add an ‘if not, why not’ clause on clawback and increase termination disclosures. |