It is not unusual for remuneration benchmarking to cause conflicts between the Board and management.

In a number of circumstances, we have seen Board remuneration committees seek independent information and advice on appropriate reward strategy and levels of fixed remuneration, while management seek information from another provider (allowed under the Corporations Act), which they interpret and provide to the committee in support of their own views and proposals.

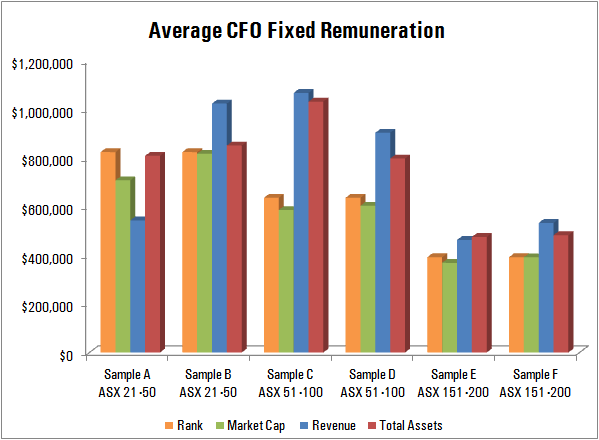

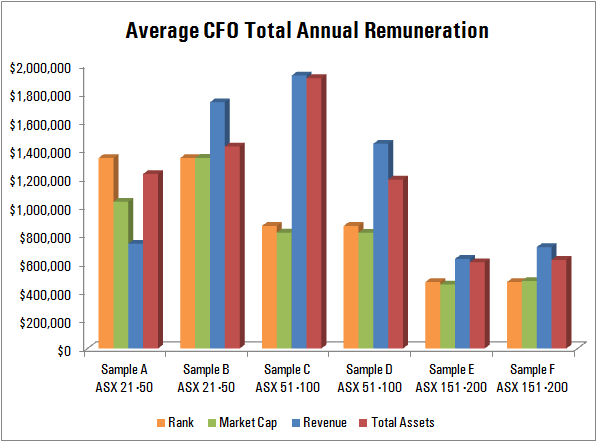

To illustrate possible conflicts that may arise in such a situation, we have completed a simplified sample external benchmark analysis (as most KMP benchmarking is horizontal not vertical, although internal relativities are always considered in remuneration reviews).

We explore data for the chief financial officer (CFO) of six companies, two each in:

- the top 21-50 companies;

- the top 51-100 companies; and

- the top 151-200 companies,

with companies ranked by market capitalisation. The highest ranked company in each sample had a market capitalisation from 2.8 times (21-50) to 1.8 times (151-200) the lowest ranked company.

For each of the six companies, we compiled information on fixed remuneration and total annual remuneration (including annual incentive payments) for four comparator groups based on:

- The population of the ranked sample (Either 21-50, 51-100 or 101-200)

- Market Capitalisation;

- Revenue; and

- Total Assets.

Companies included in the analysis for the last three metrics were between half of the relevant company’s data and 50% larger.

The charts below highlight the average reward payable to a CFO using these four filters, with samples A through F representing the six companies. There was little difference between the average and median.

The charts display that using information relating to an organisation’s relative rank on the ASX can be unhelpful and achieve vastly different results to those obtained using other more specific filters. Using a customised comparator group has the potential to exacerbate this effect.

Organisations which may be similarly ranked could have very different revenues or assets, although we acknowledge that in relation to a company’s earnings market capitalisation is generally an appropriate surrogate.

Remuneration consultants will apply more than one lens when conducting a remuneration review, taking the most appropriate metrics for each organisation into account to obtain a well grounded recommendation.

Benchmarking will often be overlaid by the application of further lenses, including organisations whose operations are primarily Australasian as distinct from substantially international, or organisations in a comparable industry sector.

Further considerations

The issue we have highlighted is far from the only conflict likely to be encountered during benchmarking assignments. In discussions with both management and members of remuneration committees, we are observing a significant number of challenges arising from:

- Varying perspectives regarding the most relevant benchmark sample, which may be companies with comparable revenues or assets under management or may be industry specific, a customised company benchmark, a broad ASX index or a blend of local and international companies;

- A different interpretation of the same data;

- Omissions in clarifying the assumptions used;

- Varying interpretations when management or Board seek a prospective as distinct from a retrospective view of market award levels;

- A blurring in some instances of whether payments under a retirement plan or legacy benefit plans are included or excluded when describing fixed remuneration.

- The basis of allocation of share rights (see our article here on this matter).

- Confusion around awards realised under long term or annual incentive plans, which are at variance with values reached by accounting treatments and the values of target awards or maximum awards.

- Varying views on the degree of difficulty of long term incentive plan hurdles for example:

- Does full vesting occur after three, four or five years?

- For EPS performance standards, does 50% vest at 5% compound and 100% at 10% compound or does 20% vest at 10% compound and 100% at 15% compound?

- For relative TSR performance standards, does 50% vest for relative performance above the 50th percentile of the comparator group or does vesting commence at the 50th percentile? Does 100% vest for relative performance above the 75th percentile or 100% vests for performance above the 90th percentile?

- Erroneous assumptions that executives receiving fixed remuneration at the median are also receiving annual incentives and long term incentives at the median – they may be receiving incentives at well above or well below the median. (Most survey tables represent a discrete sample. For annual incentives and long term incentives, samples normally represent a distribution where less than 100% of the executives have received an award in the current year. Hence, the distribution of information on both the annual incentive and the long term incentive often represents an analysis of award values for recipients and excludes zero values.)

Conclusion

Since the publication of remuneration information in Annual Reports, the amount of information available for benchmarking purposes has increased significantly, as has its complexity.

We have observed that some organisations claiming to have a fixed remuneration policy at the median have over time elevated their fixed remuneration well above the median, either due to incremental increases with increased executive tenure and improved performance or the expansion or contraction of the company in regard to a particular metric. When on plan annual and long term incentives are taken into account, total reward levels are actually in the top quartile.

Remuneration Committees should ensure that they do not make claims which cannot be substantiated due to flawed or oversimplified benchmark practices.

In interpreting reward data, either developed internally or provided externally, Boards need to be assured that the criteria used in sampling is the most relevant for the company. It is appropriate for an Asset Manager to place less reliance on organisations with comparable revenues, though in another setting annual revenues may be far more relevant than assets managed. In this context, we are observing major retailers would use gross profit margin as a surrogate for revenue not total revenues when exploring comparators outside the retail environment.

If a broad-based index (eg S&P/ASX 100) minus selected exclusions is used as a comparator group, it is important that organisations are transparent about which companies have been excluded and why. Consistency year-to-year on the method of choosing the customised comparator group is also important. Boards must also be cognizant of the fact that the smaller the comparator group, every company that is included or excluded will potentially make a large difference to the resulting analysis.

It is necessary for Boards to carefully examine total reward, not elements of reward in isolation of the other core components, and in this context the three critical ingredients would be:

- fixed remuneration;

- annual incentive award outcomes and/or annual incentive award opportunity; and

- long term incentive award value using a common methodology.

Information providers to management and advisers to Boards need to ensure their sample is thoroughly considered, that the distribution of accountabilities among the key management personnel population is understood and that their interpretation of relevant market information is overlaid with organisation, industry and geographic specific insights.