Benchmarking has become indispensible in today’s remuneration review process. Unfortunately, like any tool, the growth in its use is only matched by the growth in its abuse. In remuneration, there are few inexorable truths.

This is partly because any remuneration statistic will be based on assumptions. What these assumptions are will depend on the organisation that created the dataset. It is also due to the nature of work – few roles can be perfectly correlated as every position is slightly different.

It takes years of experience to understand and be able to compare data in the context of both organisation structure and operating metrics.

To illustrate, here are a few of the complexities that an experienced remuneration consultant will consider:

1. Gathering and calculating data

All consultants will work from the same or similar data, but their statistics for the same group of companies – say the ASX 50, ASX 100 or ASX 200 – will not be the same. Some of the reasons for this include:

a) Inclusions and exclusions

In order to make sure the data is comparable, remuneration consultants may decide to exclude certain datapoints from a dataset.

· Tenure

If an executive leaves part way through the year, do you annualise the pay the executive received for the portion of the year they served? Do you go back to the last full year’s pay for the executive or the last person in the executive’s role? Or do you simply exclude that executive’s data from your dataset? If an executive changes role part way through the year do you include the pay under one of the positions or do you exclude them?

Do you use the intended fee if the Chairman or Director has not served a full year and if so, do you use annualised committee fees? Do you ignore the fee schedule entirely? If fee levels change during the year, do you record the new fee arrangements annualised?

The number of KMPs who change roles during the year is not negligible. Recently released research by Booz and Co placed CEO turnover at 23% for 2011 and 15% for 2012.

· Residence

If an executive is living overseas and is paid commensurate with local peers or receives benefit payments relating to their overseas location, should their total employment cost be included in a dataset for Australian companies? Or do we simply ignore the different pay settings?

· Outliers

If an executive is so highly paid that their pay skews any statistical distribution, should they be included? Or should the exception be ignored?

b) Other Pitfalls

· Constituents of the ASX

Market capitalisation is not static. When ranking Australia’s top companies, which companies are included in each set of constituents will depend on the date the market capitalisation is measured. If one organisation measures market capitalisation at June and another in December, they will potentially be analysing a different group of companies and executives.

· Treatment of equity payments

Do you enter the figure in the statutory table for equity payments? Do you record the number of shares or options granted and use that to calculate a value? If so, how do you calculate that value? Do you use a proprietary calculation, or choose a particular fair value calculation or use the face value of the equity? If there is no grant date or no price disclosed for the shares, what price do you use to carry out any calculations? What assumptions do you use for expected growth, volatility, and so on?

Do you treat long term incentive equity in the same way that you do short term incentives deferred into shares or simply paid as shares? Do you use the actual payment tables currently appearing in many companies’ annual reports? Do you include or exclude dividends on fully paid shares held in escrow?

· Position ambiguity

If there is an Executive chairman and a CEO, who should be considered as the head of company? If there are joint CEOs, should they be added together to make one CEO, should one be included, or should both be included as joint data points? For other roles that don’t fit exactly into a standard box, how do you record them?

· Bands

In countries where bands are used, such as New Zealand, do you take the middle of the band, the top of the band, the bottom of the band?

2. Comparing Data

Choosing companies against which to benchmark is complicated due to the relatively small scale of the Australian economy. The position is even more restricted when considering the number of comparable organisations (based on revenue, assets, enterprise value, employee numbers or industry sector) against which position benchmarking is valid without interpretation and supplemental advice.

a) What metric to use?

What are the key criteria for comparison? Is it annual revenue? Is it total assets, net assets, operating profit, market capitalisation or a combination of the above? Perhaps investment returns and or funds under management are more relevant for an investment company?

A number of Proxy Advisers indicate that the most relevant foundation for pay comparison is market capitalisation, that is, relative ASX/NZ rank. Many consultants would use revenue. Some would use a composite of revenue, assets managed and market capitalisation or enterprise value.

While market capitalisation has a common foundation, we consider that comparing total revenues across industries and sectors is not valid. Gross revenue of a financial institution or a bank is different from that of a manufacturer and again, different from that of a wholesaler or retailer. Total assets managed in an investment/banking environment are different from those in manufacturing, construction or a resources company.

For example, for a bank Egan Associates would consider revenue as the sum of net interest income, fees and investment returns, not gross revenue including the cost of goods, which in the case of a bank is interest on deposits or borrowings. For a retailer where inventory is often funded for 90 or more days by suppliers, the primary revenue metric is gross margin, which will vary depending upon whether the retailer is in high unit price fashion goods, white goods, brown goods or staples.

In this context it is not surprising when looking at different investments and management reward, Proxy Advisers and others use market capitalisation and profit as a primary foundation for reviewing executive pay. It must be noted that comparisons using market capitalisation can involve companies that have few similarities in terms of industry, risk, revenue and/or locations. In this context benchmarking is critical though the number of ideal benchmarks is likely to be limited.

There will be opportunities for comparison which may not be being considered by many providing information and a number of Boards may not question information that they receive.

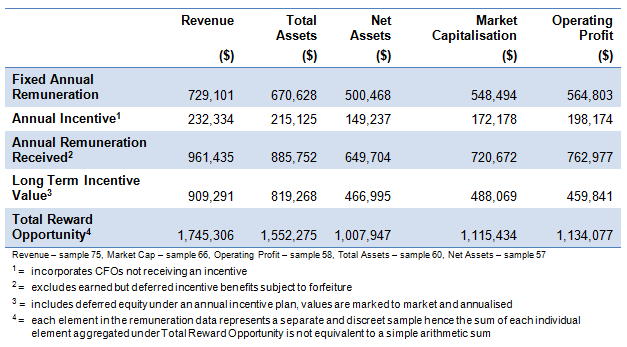

The table below provides information which we recently extracted as part of a KMP Benchmark study. It highlights each of the metrics relevant to the organisation for the position of Chief Financial Officer, and as a consequence the challenge in providing a remuneration recommendation where each metric considered offers a different answer. The table provides the average for each element of reward.

b) Use of the same metric for each role

Should core metrics of a company apply to all positions in terms of benchmarking?

Are the metrics relevant for the position of Chief Financial Officer similar to those for the balance of the C-Suite including the CIO, CSO, CRO, CMO, Head of HR and General Counsel? Do they differ from the Chief Executive Officer? Is the Head of a major Business Group benchmarked in relation to the scale of the Business Group or the company within which the Business Group sits?

c) Widen the net

Do the breadth of geographies and jurisdictions the company operates in have any relevance in benchmarking?

There are some companies whose global operations make it meaningful to extend comparisons to organisations based overseas. This is a judgement call, with the answer often depending upon the industry, the nature and location of operations and the breadth and depth of the accountabilities of each individual position. Benchmarking can also be influenced by factors such as the maturity of the industry and the company, the development profile and aspirations of the company, as well as its stated reward strategy – that is does it have heavy reliance on fixed remuneration or at risk incentives and, in the latter category, is the emphasis on annual cash-based incentives or equity-based longer term incentive horizons.

Given the ever-increasing complexity of supporting management and Boards, particularly the latter, it is important to note the difference between service providers offering information such as benchmarking data and those who are willing to present a remuneration recommendation. The nature of the provider’s engagement often reflects both their expertise and their intimacy of knowledge of the company.

With the passage of the Corporations Amendment (Improving Accountability on Director and Executive Remuneration) Act 2011 in late June 2011, directors’ reports of listed companies now have to include details of any remuneration consultants they use and any remuneration recommendations (as defined in the Act) provided by those consultants.

This has contributed to the focus of many firms shifting more to the provision of information rather than recommendations. Recent disclosures reveal that many Boards are not receiving and/or seeking recommendations but rather data to meet their governance obligations.

The nature of service being provided by external firms is reflected in their communications to clients, often published in remuneration reports, where many either acknowledge that they are providing a recommendation or alternatively clearly state that their reports do not contain a remuneration recommendation in relation to key management personnel as defined by Division 1 of Part 1.2, Chapter 1 of the Corporations Amendment (improving accountability on Director and Executive remuneration) Act 2001.

We also note arising from these legislative changes that management in support of the Chief Executive will often approach remuneration specialists for information but not a recommendation in order that the relationship is not in breach of the Corporations Act.

Providing information without a series of filters is unhelpful in the majority of settings due to all of complexities we have outlined above. The filters provide an understanding of the data in the context of either a derivative of a work value assessment or a working knowledge of the structure and distribution of accountabilities among comparator companies.

Egan Associates has built its reputation on its in depth knowledge of the employment and retention challenges faced by Boards in varying industries and at different stages of development and prosperity. We have always possessed the expertise and courage to prepare recommendations.

Benchmarking is more than you think and it is particularly important that you do think through your information and advice requirements.