Today an increasing number of Remuneration Reports reveal the proportion of reward split between fixed remuneration and potential earnings under incentive programs. The method of disclosing this proportion varies significantly.

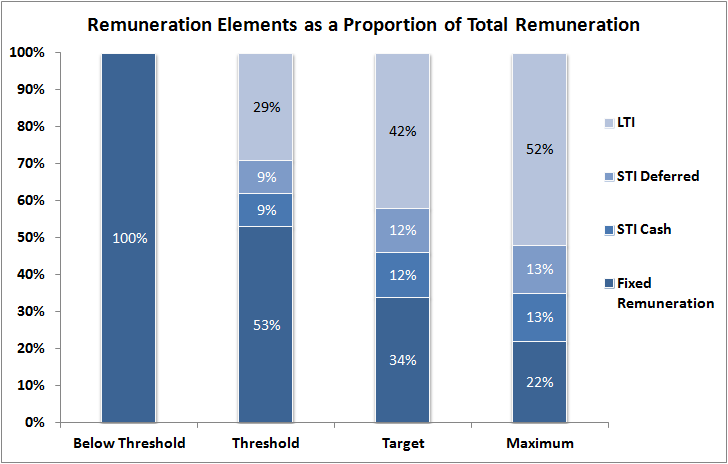

A standard approach is to disclose the opportunity provided at target performance under short-term and long-term incentive plans (STI and LTI) as a proportion of total remuneration. The figure below is an example of this.

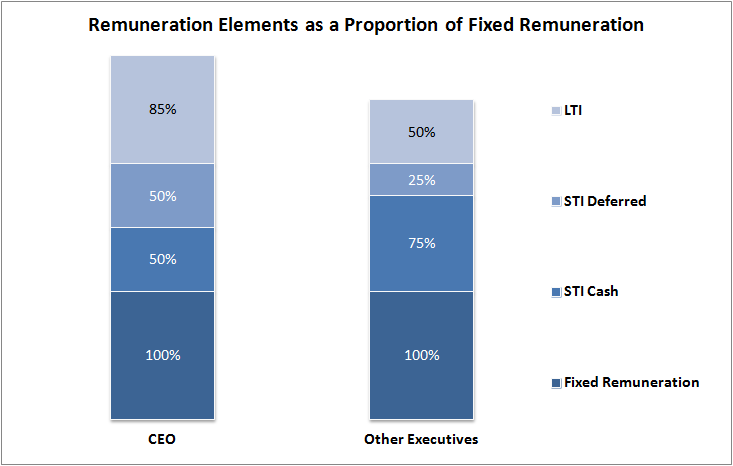

Another approach, which may be clearer to certain shareholders, is to identify the STI and LTI opportunity at target as a proportion of fixed remuneration, as shown in the example below.

The above two approaches may also be used in combination.

However, neither of these approaches provides information on how the remuneration mix changes at different performance levels. Some companies provide a comprehensive and all inclusive graph of reward outcomes, as shown in the graph below of a CEO’s remuneration mix for varying levels of performance. Note that in this case the long term incentive grant is influenced by the annual performance.

Such a graph can also be paired with another that portrays remuneration dollar values instead of percentages, to give a quick overview of how much an executive is due to receive at different levels of performance.

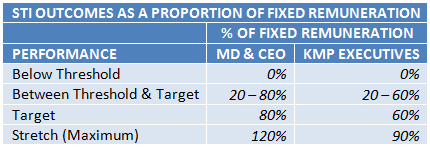

Other companies may rely on additional tables to provide information on the proportion of the annual incentive opportunity as a proportion of to fixed remuneration at threshold, target and maximum. For an example, see the table below.

Another standard approach for disclosing this information is in footnotes or text, although this makes it more difficult for shareholders to gain an overview.

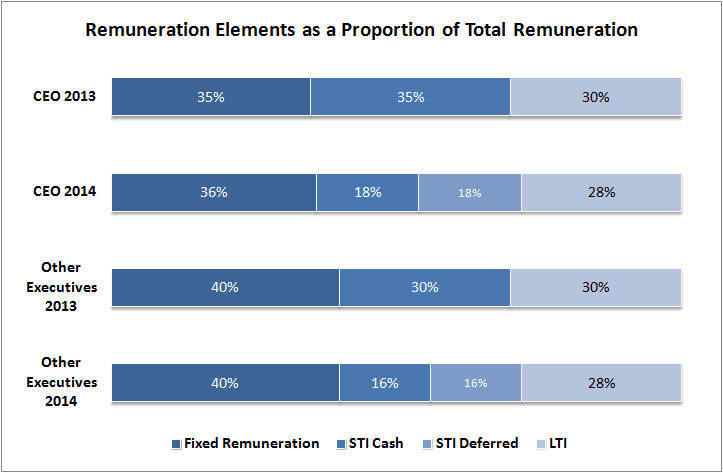

Some companies use remuneration mix illustrations to juxtapose the current year’s balance of remuneration elements with that of future years when remuneration structures are in transition. This is shown in the target remuneration mix example below, where a deferred STI element has been added to the remuneration structure.

Observations

These illustrations highlight different ways of communicating remuneration opportunities to shareholders. Although we note that pictorial representations can enable better understanding for retail investors, we do not favour one method over another. Most important to shareholders is that whichever style companies use to communicate their remuneration mix, they include information on:

- The proportion of incentive payments to fixed payments if threshold performance, target performance and maximum (stretch) performance is achieved.

- The basis for the allocation of deferred STI, including:

- How much of the award is deferred?

- What is deferred? (Cash, restricted shares, rights, options?)

- If it is equity, how is it valued for allocation? (For example, the volume weighted average share price (VWAP) for the five days prior to the incentive approval)

- The underlying basis for determining value when allocating the long term incentive. (For example, the VWAP for the five days prior to the grant, or an accounting model such as Black Scholes or Fair Value that accounts for future dividends)

This will ensure shareholders have all the information they need to understand the true proportion of incentive payments to fixed remuneration at different levels of performance and that the illustrations accurately reflect reward paid or the financial reward opportunity potential.