Last month we outlined some of the complexities of tracking total shareholder return (TSR) that can lead to issues with the assessment and verification of employee entitlements. We promised to further examine selected issues with a series of illustrations.

This month we look at the issue of smoothing.

Smoothing is used to provide a better representation of the company’s actual performance, such that vesting of executive entitlements does not depend on day-to-day share price volatility. Smoothing won’t alter the results of the peer performance group, but will enable more representative comparison of the company’s performance.

Companies will often use 22-day smoothing, but if their share price is particularly volatile (for example if the business is affected by a commodity price cycle) 60-day smoothing can be used.

The danger of extending smoothing to 60 days and beyond is that the longer the smoothing period, the more likely that the final result of the peer group and the sample company will be affected by market-based forces such as dividends, corporate actions, refinancing and M&A. This may distort results.

It is important to make an informed decision at an early stage as to what level of smoothing will be used to measure relative TSR performance.

To see the difference this decision can make, we look at two companies which we will call A and B. Let us assume that they both have a vesting profile where 50% of their equity vests at the median of the peer group (in this case we’ve chosen the ASX300) and 100% at the 75th percentile.

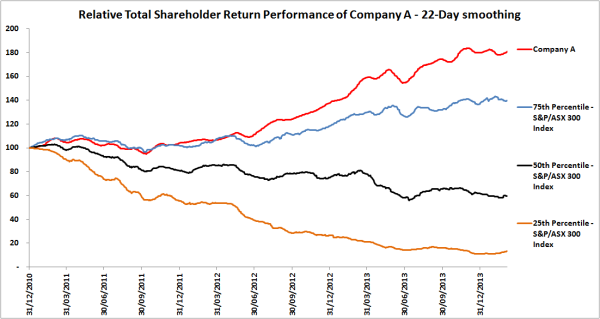

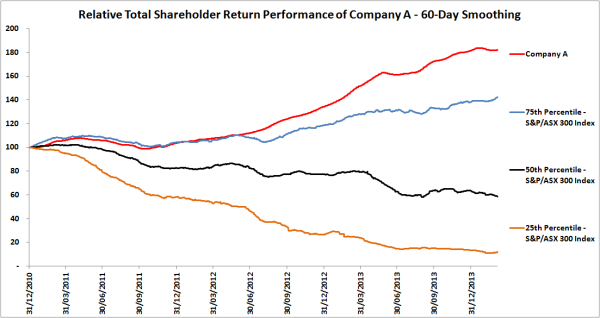

Company A’s performance compared to the performance of the peer group can be seen in the graphs below, the first using 22-day smoothing and the second using 60-day smoothing. (Company A is depicted in red. TSR is rebased to 100 at the beginning of the period.)

The position of the sample company at the end of the performance period relative to the index is the same for both types of smoothing.

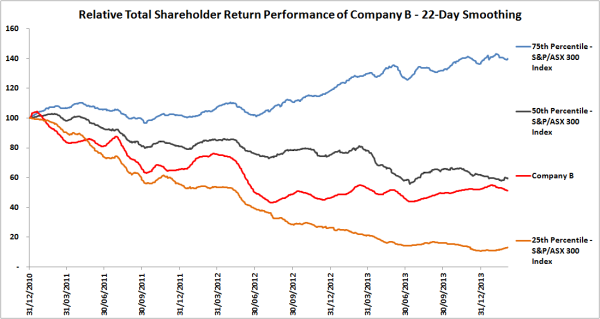

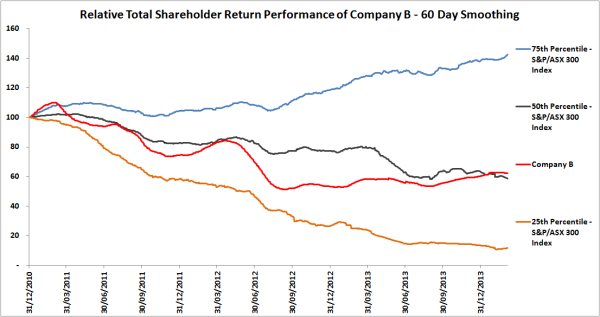

This is not the case for Company B, also depicted as a red line in the graphs below:

As can be seen, there is a large difference in final ranking between the two types of smoothing – company B falls below the median using 22-day smoothing, but above the median for 60-day smoothing. For the given vesting schedule, the choice of smoothing will be the difference between equity vesting and no equity vesting.

So which type of smoothing is the correct choice for the organisation?

Egan Associates’ analytics function supports clients in this area, providing advice on what is most appropriate for the organisation.

We provide a benchmark analysis service for relative TSR to determine the percentage of rights/options which vest and verify Board and/or Remuneration Committee decisions to vest securities. We also monitor relative TSR performance over a series of grants on a quarterly or six monthly basis as requested by clients to inform the Board, Remuneration Committee and key executives how performance is tracking against TSR hurdles.