The Australian Council of Superannuation Investors (ACSI) has released a report which has made some interesting observations about the discrepancy between the statutory reporting of executive pay and the pay the executive actually takes home.

ACSI singled out Tony Poli, the Executive Chairman of Aquila Resources, for attention, because his base pay was one of the ten lowest for a CEO in the ASX 101-200. The CEO’s cash pay was $572,000 in the 2011 year, but he also exercised 5 million options which had been approved at the 2005 AGM and received 19,166,400 shares, amounting to a total value at the time of $169,360,199.

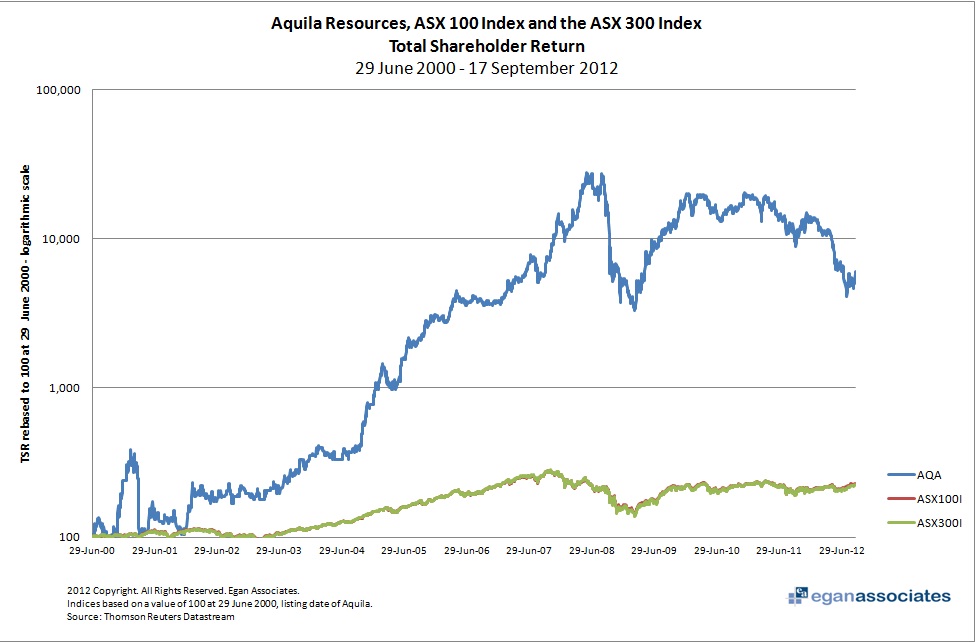

We have looked more carefully at the history of the last 12 years’ issuance of securities to Tony Poli, Executive Chairman of Aquila Resources.

We believe that the research commissioned by ACSI is comprehensive, clearly represents a longitudinal analysis and reflects on key areas that Directors, and particularly those chairing Remuneration Committees, need to address when applying various valuation methods at the time of issuing securities under a long term incentive plan.

We believe that the analytics embraced and the explanations offered in the ACSI Report are clear and do not endeavour to distort. The report has obviously identified Aquila Resources as an outlier.

Since Aquila’s listing, Poli has been granted two tranches of 5-year options. At the time of listing he received 12.5 million options over ordinary shares at an exercise price of 40c and at the expiry of that 5-year period a further 5 million options were issued at an exercise price of $4.

The ultimate number of securities progressively granted reflected adjustment for bonus issues offered to shareholders over that intervening 10-year period with the most significant being a 1:1 bonus issue in the 2008 financial year. This is a common strategy in a minor resources company to both attract investment and reward for success.

The real challenge for less sophisticated investors in such a situation is keeping up with actual wealth creation (the difference between the market value of shares that the options ultimately convert to and the exercise price for the relevant options).

Accounting fair value (option valuation) methodologies could never “keep up” in a rising market, especially for such junior miners with volatile underlying asset prices and revenue streams. Black Scholes was used for Poli’s initial options grant and then a binomial valuation when subsequent option grants were subject to performance conditions (share price growth hurdle and commitment to a feasibility study).

While the rewards have obviously been substantial, it should be noted that for every $100 invested at the time of the company’s listing in 2000, the current market value for that investment is $6,000 and, at the peak prior to the GFC, every $100 invested in the company had a value of $28,000.

If one examines the return over the same period among Australia’s top 20 companies, the multiplier in shareholder return for $100 invested would be far less significant.

From a shareholder’s perspective we believe these accomplishments and the benefits flowing to an earlier investor in the company should be encouraged.

ACSI has neither specifically commented on the obvious entrepreneurial attributes of the CEO, nor the fact that while he has been a beneficiary of the company’s success, Poli also retained securities issued under the company’s incentive plans for the entire duration of their life, exercising those securities in the final month before they expired.

It should also be noted that the Executive Chairman made substantial personal investments in the company at the time of joining and drew a modest cash salary, clearly being committed to the opportunity and, along with other shareholders, retaining his equity rather than cashing out at the market’s peak.

Aquila Resources has also been fully transparent in its disclosures, which will be observed in the table below, which is a snapshot of the 2011 remuneration report.

While this case represents an outlier where a company has experienced success (though clearly also a dramatic decline in value since the GFC), the ACSI Report highlights some underlying concerns that some companies may not have been as transparent as Aquila.