The Australian Prudential Regulation Authority (APRA) has released Draft Prudential Standard APS 330 Public Disclosure implementing Basel Committee on Banking Supervision remuneration disclosure requirements.

One section of the standard mandates remuneration disclosure for senior managers and material risk-takers at authorised deposit-taking institutions, adding to the current requirement under the Corporations Act for organisations to disclose remuneration information for key management personnel.

The disclosures, set out in Attachment E of the Standard, are broken down into qualitative and quantitative disclosures.

Quantitative Disclosures

Information should be provided on:

- The body overseeing remuneration for the organisation

- Any consultants engaged to oversee remuneration

- The types of employee considered as risk takers and senior management

This disclosure also requires information on the organisation’s remuneration policy, encompassing details such as:

- policy scope

- review schedule

- risk overview, measures taken to account for risks, and treatment of risk and compliance employee remuneration

- deferral and clawback policies for ensuring longer-term performance

- description of variable remuneration elements and remuneration mix

- explanation of links between performance and remuneration

- external consultants overseeing remuneration, the types of employee considered as risk takers and senior managers

Quantitative Disclosures

Data should be provided on:

- The number of meetings held by the body overseeing remuneration, and member remuneration.

- Number and total amount (aggregate) of sign on awards, severance payments and guaranteed bonuses awarded during the year and the number of employees receiving a variable remuneration award during the year.

- Total amount (aggregate) of deferred remuneration paid and outstanding deferred remuneration, split into cash, equity and equity linked instruments.

- Quantitative information on the total amount of deferred and retained remuneration exposed to implicit (eg share price change) or explicit (eg clawback) adjustments and the total number of reductions due to those adjustments.

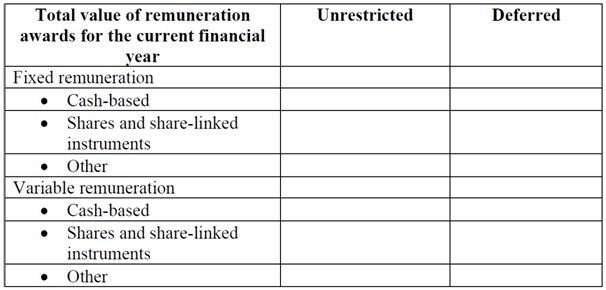

- A table summarising the remuneration awards as seen below.

APRA has suggested that the requirements should start for reporting periods beginning on or after 30 June 2013. They are to be published on the organisation’s website with the same frequency of audited financial accounts or the lodgement of financial statements under the Corporations Act for unlisted organisations.

According to the standard, a senior manager includes:

(a) an executive director;

(b) a senior manager, being a person (other than a director) who:

(i) makes, or participates in making, decisions that affect the whole, or a substantial part, of the business of the ADI;

(ii) has the capacity to affect significantly the ADI’s financial standing;

(iii) may materially affect the whole, or a substantial part, of the business of the ADI or its financial standing through their responsibility for:

- enforcing policies and implementing strategies approved by the Board of the regulated institution;

- the development and implementation of systems used to identify, assess, manage or monitor risks in relation to the business of the regulated institution; or

- monitoring the appropriateness, adequacy and effectiveness of risk management systems; or

(iv) a person who performs activities for a subsidiary of the regulated institution where those activities could materially affect the whole, or a substantial part, of the business of the regulated institution or its financial standing, either directly or indirectly (but not for a subsidiary that holds an RSE licence under the Superannuation Industry (Supervision) Act 1993).

According to the standard a material risk-taker includes:

Other persons for whom a significant portion of total remuneration is based on performance and whose activities, individually or collectively, may affect the financial soundness of the ADI.

Employees employed directly, retained under contract or employed by or a contractor of a body corporate that is a related body corporate of the ADI are included.