The European Union this month agreed to cap bonuses for bank executives to a maximum of twice fixed pay, with implementation slated for 2014. According to the Council of the European Union:

Bonuses will be capped at a ratio of 1:1 fixed to variable remuneration, i.e. bonuses are equal to fixed salary. This ratio can be raised to a maximum of 2:1 [with a shareholder vote] … For the purposes of applying this ratio, variable remuneration may include long-term deferred instruments that can be appropriately discounted. The European Banking Authority will prepare guidelines on the applicable discount factor, taking into account all relevant aspects, including inflation rate, risk and appropriate incentive structures. Moreover, the long-term instruments have to be fully “claw-back-able” and “bail-in-able”.

It is not clear whether the long-term deferred instruments referred to as being a part of the “bonus” will cover only deferred annual short term incentives or also traditional long term incentives.

The cap has emerged from concerns about the quantum of pay bank executives receive and the fact that potential bonus payments may encourage executives to take on significant risk. It is believed this played a role in the global financial crisis, which is why the EU is focusing on the financial sector.

Data released in September 2012 from the UK Office of National Statistics showed Financial sector employees took home 36% of the aggregate of UK bonuses for the 2011-2012 financial year, although the total amount of bonuses had fallen 35% since 2007-2008, when the global financial crisis first reared its head.

Given Europe’s focus, Egan Associates believes it is an appropriate time to reflect on the level of bonuses over the last three years in the ASX 100 financials sector compared to other sectors. Due to the uncertainty of how long term incentives will be handled under the EU plan, we have limited our examination to short term incentives.

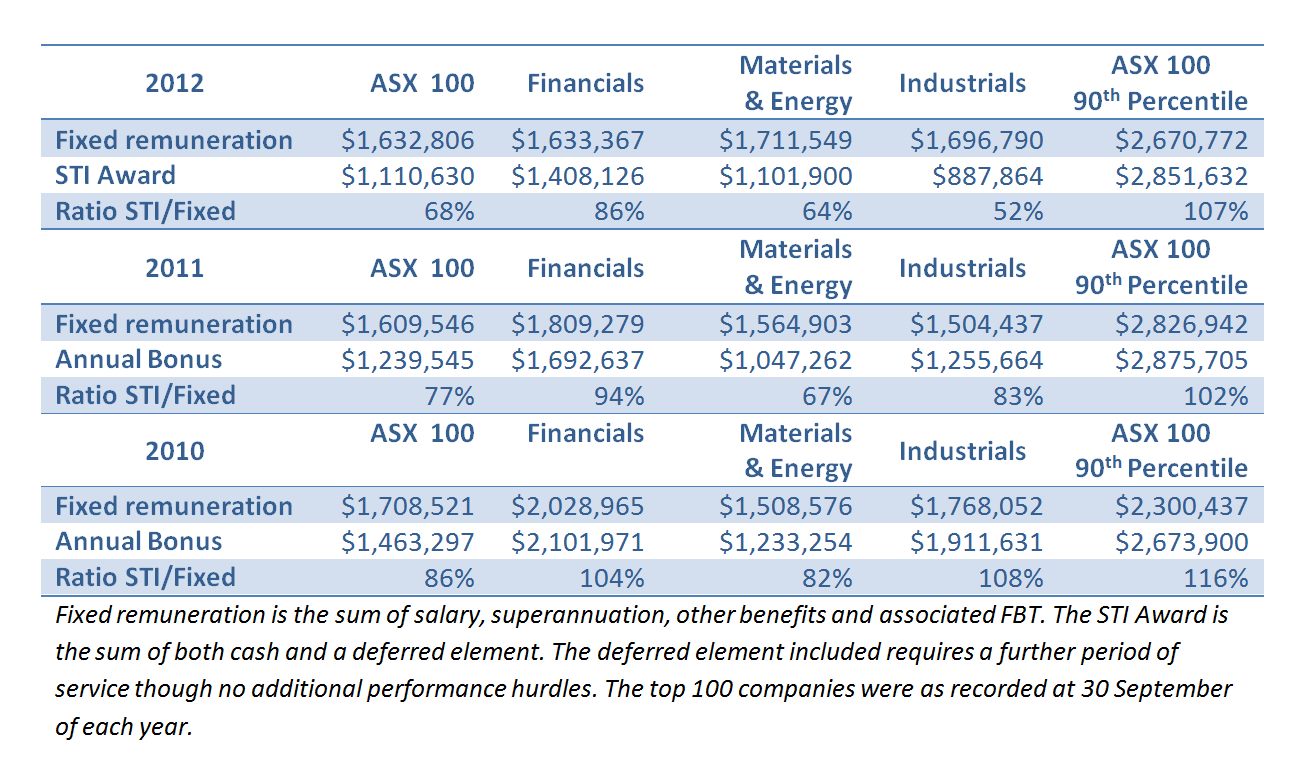

CEO

The table below displays the average fixed remuneration and STI award amounts for CEOs in Australia’s top one hundred companies, both as one group and broken down into sectors. It also includes the 90th percentile fixed remuneration and STI awards for the top 100 companies in aggregate.

Click to enlarge

The average STI award for CEOs in the financial sector was higher from 2010 to 2012 than the average for the whole of the ASX 100 and higher than awards in the Materials and Energy and Industrials sectors.

This is despite the average value of STI awards for financial sector CEOs declining by more than 30% over the same period. The Materials and Energy sector has seen a 10% decline in the value of STI Awards, while the value of STI awards for Industrials has halved.

Egan Associates has observed a recent reduction in the maximum award available under STI plans, which reflects Board initiatives to manage reward levels. Companies are, however, continuing to reward their executives well for exceptional performance, with STI awards at the 90th percentile increasing from 2010 to 2012 by 7%.

The number of Australian CEOs deferring a portion of their short term incentive award has been on the rise since 2010, moving up in the ASX 100 from 27% to 37%. The exception is the Financials sector, where 50% of executives who received a bonus had a portion of it deferred.

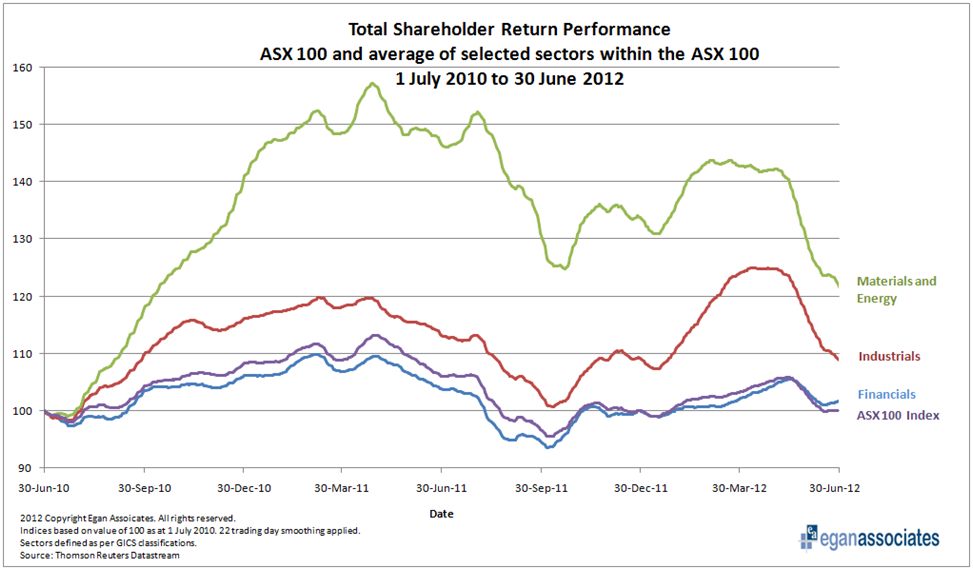

Like the average short term incentive award, average CEO fixed remuneration has fallen since 2010 for all of the sectors we examined except Materials and Energy, where there was a 13% rise. Materials and Energy did produce a better total shareholder return over the two years from 30 June 2010 to 30 June 2012 than the other sectors studied.

Click to enlarge

Neither the average nor the 90th percentile figures for short term incentive awards have exceeded the EU’s maximum 2:1 variable to fixed ratio. If the rule only considered short term incentives, most Australian CEOs could be paid under prevailing STI plan parameters within the EU regime, especially given deferred bonuses will attract a discount factor. However, in order to be paid an STI award of over one times annual remuneration, shareholder approval is required under the EU’s initiative. This effort could dampen some STI awards, or result in the lifting of fixed remuneration.

If “bonus” also includes long term incentive awards, the amount of variable remuneration included in the bonus side of the ratio would be much higher, especially if considering realised value rather than a fair value estimation of how much grants might be worth. We will consider this further at a later date.

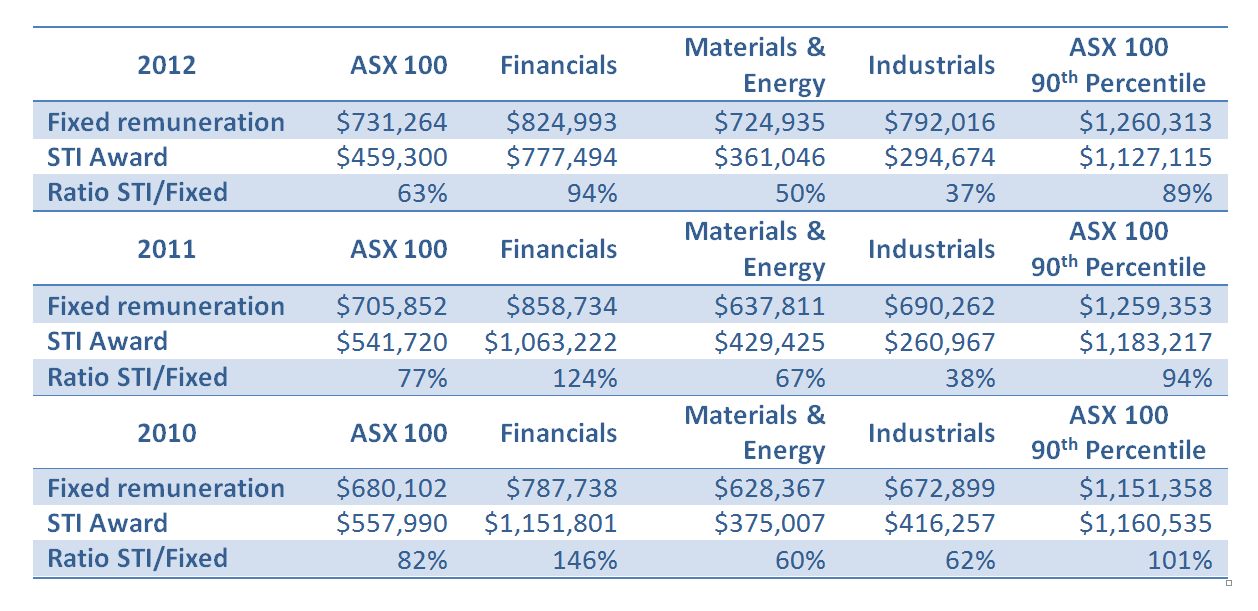

Top 5 Executives

We repeated our analysis for the top five highest paid executives other than the CEO of the top one hundred companies.

Click to enlarge

The difference between the STI award levels in the Financials sector and the other sectors was more pronounced over the three-year period for the top five executives than it is for the CEOs, with financial sector executives receiving over twice the award which Materials and Energy and Industrials executives received in 2012. The STI award fell from 2010 to 2012 by 33%, 3.7% and 29% in the Financials, Materials and Energy, and Industrials sectors respectively.

While CEO fixed remuneration stagnated from 2010 to 2012, the top five executives enjoyed pay rises, with the averages for the Materials, Energy and Industrial sectors rising more than 15% from 2010 to 2012. In our judgement, this difference reflects in part Boards taking the opportunity to replace long-serving CEOs at lower levels of fixed remuneration either internally or externally and secondly, increased competition for the CEO’s direct reports as many leading companies embark upon transformational initiatives following the global financial crisis.

Comparing the fixed remuneration to STI awards for top 5 executives, in 2012 even those executives paid at the 90th percentile did not receive more than their fixed remuneration as a short term incentive award payment. As with the CEOs, it is clear performance hurdles have become more challenging as the economic environment tightens.

Conclusion

It appears clear CEOs and executives are currently not being paid excessively high amounts of short term incentive in comparison to their fixed remuneration. It is important for remuneration committees to ensure the ratio of maximum STI awards to fixed remuneration remains within bounds acceptable to shareholders while retaining sufficient flexibility to reward outperformance. The area we believe requires more attention is the maximum benefit received by executives under long term incentive plans, which is possibly addressed under the EU’s scheme. We will consider the bonus cap more thoroughly once additional information is available and will be interested to explore the effects of its implementation.

We suspect it could result in some or all of the following:

- Higher fixed remuneration;

- A higher proportion of deferred awards with longer deferral periods; and

- An exodus of talent to markets without payment limits.