Issue 22 – February 2018

Contents

- Wages & Employment

- Recent Profit Growth Sector Variability

- Future Profit for Sharing

- Conclusion

Wages & Employment

In our January Newsletter we highlighted the workforce setting in Australia with a number of international comparisons regarding recent wage increases.

The latest Average Weekly Earnings (AWE), and Wage Price Index (WPI) figures held some good news for the economy. The Australian Bureau of Statistics revealed a 0.6% seasonally adjusted wages increase reflected in the Wage Price Index. They further reflected that the wage price index rose by 2.1% over the 2017 calendar year while concurrently revealing that wage movement in the final two quarters of the 2017 financial year recorded a rate of improvement reflecting falling unemployment and underemployment rates in parallel with increasing job vacancies.

Of some greater concern to the corporate sector would be that seasonally adjusted private sector wages increased by 1.9% compared to the public sector of 2.4% over the past 12 months. The data also revealed that wage growth in the 2017 calendar varied by sector ranging from 1.4% in the mining sector to 2.8% in the health care and social assistance sector.

The WPI data also revealed that wage growth varied across sectors with the mining industry wages increasing by 1.4% compared to 2.8% in the healthcare and social assistance sectors. It also revealed, on a regional basis, that Victoria experienced the highest annual wage growth of 2.4% with the Northern Territory reporting the lowest at 1.1%.

While there appears to be a greater propensity in the public sector for an uplift in wages, tighter reigns are being applied in the private sector which has an obvious and clear focus on obtaining an appropriate return on capital and rewarding shareholders for their investment risk.

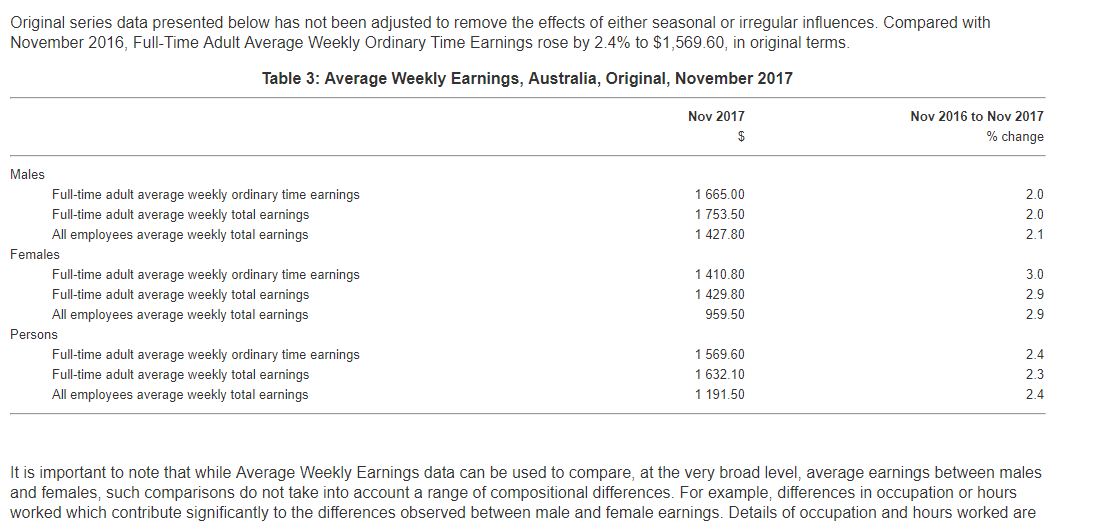

The ABS found that in the twelve months to November 2017, Adult Average Weekly Ordinary Time Earnings rose by 2.3% to $1,567.90. These figures are a slight increase on the previous twelve months (2.2%) and a significant increase on the 12 months before (1.7%). The full-time Adult Average Weekly Total Earnings in November 2017 were $1,628.10, a rise of 2.2% from the same time last year. These figures also show a slight upward trend. Female average earnings rose by 2.9 per cent to $959.50 during the period, whilst the average male weekly earnings grew 2 per cent during the same period to $1427.80.

All employee average weekly total earnings in the public sector increased by 3% compared to 2.3% in the private sector, the national figure being 2.4%.

It is important to note that the AWE deals with a wider range of factors compared to the WPI. The ABS define these factors as those which can contribute to compositional change, and include variations in the proportion of full-time, part-time, casual and junior employees, variations in the occupational distribution within and across industries and variations in the distribution of employment between industries. The average weekly earnings differential between men and women remains significant, though much of the difference can be attributed to a higher rate of part time work amongst women. As they stand, AWE statistics cannot clarify the extent to which men and women receive equal pay for equal work, nor the reasons for any difference. It is also worthwhile bearing in mind that the AWE report is affected by the split of males and females working in different industries.

ABS Chief Economist, Bruce Hockman, stated ‘The annual rate of wage growth has increased for the second consecutive quarter reflecting falling unemployment and under-employment rates and increasing job vacancy levels”.

Notwithstanding the positive aspects of the recent disclosures from the ABS, the Reserve Bank’s Assistant Governor, Luci Ellis, in a recent presentation indicated that the unemployment rate reveals that the labour market still retains spare capacity which, in itself, will have a dampening impact on wages growth. Spare capacity incorporates not only the unemployed by the under-employed.

The recent release of data from the ABS in relation to Average Weekly Earnings, reveals continuing differentials between States with the ACT dominated by public sector employees being the highest paying region, followed by Western Australia, with a significant resources sector.

Source: Australian Bureau of Statistics

The rate of increase by region, as reflected above, differs from full time adult average earnings with the highest paid regions being the Australian Capital Territory and Western Australia with the figures being $1,803.10 and $1,742.80.

Notwithstanding differentials in the annual movement of average weekly earnings in the 12 months ending November 2017 or the adjustments to the wage price index, there remains a conservative outlook in relation to future growth.

The table below highlights the current earnings differentials between industry sectors, as distinct from regions.

Source: Australian Bureau of Statistics

Source: Australian Bureau of Statistics

Average weekly earnings in the mining industry stood at $2,580.70 whereas earnings in the accommodation and food services sector stood at $1,112.90. All employee average weekly total earnings in the public sector increased by 3% compared to 2.3% in the private sector, the national figure being 2.4%.

The government is suggesting that as unemployment falls, wage growth will start to rise. They also believe that proposed company tax cuts will increase wage growth.

Concurrently, the Unions are lobbying to raise the minimum wage, after the Fair Work Commission awarded a 3.3 per cent increase in mid 2017.

James Pearson, the Chief Executive Officer of the Australian Chamber of Commerce and Industry said, “It’s early stages, but this could be the start of a gradual pick-up following recent strong jobs growth.” He also added that if the economy continues to strengthen then wages growth will increase.

The Governor of the Reserve Bank, in a recent presentation, indicated that unemployment will fall faster than previously forecast, but the bank does not expect core inflation will increase to levels in its target range of 2% to 3% before the middle of the 2019 calendar year though anticipates that unemployment will fall from its present 5.5% level (December 2017) to 5.25% by mid 2018 and remain broadly aligned to that figure until 2020. These observations were reported in the bank’s most recent quarterly statement published in early February.

In forecasting unemployment and inflation, as tempered by prevailing economic conditions, the Reserve Bank reported that they believed that wages growth would also remain subdued. Their expectation is that wage growth will pick up gradually over the 2018 calendar year as spare capacity declines and the adjustment following the mining boom ends.

Implicit in the bank’s observations is the key uncertainty in relation to the labour market outlook. In this context, the bank states that it is not clear how much spare capacity there is in the labour market and how quickly it might decline. Further, they indicate that spare capacity will translate into building wage pressures which might reflect in Enterprise Agreements offering wage adjustments above the inflation rate.

Movement in the labour market’s capacity would be influenced by entry of those currently unemployed or by current participants in the work force working more hours. In this context, participation rate outcomes will depend on a number of factors including the retirement decisions of older workers, the participation decisions of women and labour market conditions for younger workers.

The bank’s view is that if participation rates do not increase as expected, employment growth is likely to be moderated. In this context, it is their judgement that the sources of expected growth in total hours worked, including a rise in participation, a decline in unemployment or an increase in average hours worked, may each impact on spare capacity in the labour market which could well increase wage growth pressures.

In exploring the ingredients which impact on pressure for wage increases, the bank has reflected on the high level of household debt, the medium term prospect for interest rate adjustments and the impact that this may have on consumption and therefore demand for labour.

In the context of observations made by politicians, economists, the Reserve Bank and the nation’s observations about economic growth and interest rate changes among our trading partners, comment has recently emerged which reflects, among many factors, on the prospect that workers should not be forced to lock away a rise in the proportion of their wage in superannuation.

This observation arose from a recent report from the Grattan Institute which indicated that amid persistent low wages growth, the current 9.5% rate is adequate to fund a decent retirement income for the typical worker and as a consequence the demand from certain quarters to increase that rate to 12%, while increasing employment cost, may be better allocated to fund a living wage for those on modest wage levels.

The table below indicates Pension income falls for low-income earners if the Superannuation Guarantee rises to 12 per cent.

These near term observations do not reflect concerns of a number of commentators who are of the view that the superannuation funds of the majority of people retiring will not prove adequate in an environment where retiring workers are living longer and will be doing so in an environment where they will be experiencing higher living costs.

Running in parallel with this research are the economic commentators who believe that politicians and business leaders need to initiate reforms which encourage innovation and productivity which in turn will enhance income prospects over the medium term. In this context, there has also been parallel discussion in relation to the criticality of education at both university and TAFE level to prepare both today’s youth and older workers for the occupations which will be in demand in future years and the coming decades.

Other comments in terms of future prosperity and capacity to pay are influenced by the employment sector including the consumer facing sector, the industrial sector, the mining sector and emerging technologies with an overlay of the capacity of those sectors to produce outcomes at competitive cost on a global footing to ensure their prosperity locally and their opportunity for generating export income.

Recent Profit Growth Sector Variability

In order to explore if there were further avenues available for the private sector while containing fixed costs Egan Associates have reviewed movement in the level of earnings before tax among the ASX 300 and within the ASX 300 by rank and industry sector.

Our research reveals in relation to listed companies reporting during the prior three calendar years (2015,2016 & 2017) the median level of profit before tax among the top 50 companies has risen from $738.4 million to $1.185 billion with the average profit increasing from $1.877 billion to $2.618 billion.

Among the second 50 companies at the top 100 the median level of profitability has increased from $180.7 million to $251 million and the average profit from $151.22 million to $324.19 million.

Among the second 100 company’s profitability over the 3 year period has increased from $45.85 million to $77.63 million and the average from $20.73 million to $54.86 million.

Companies ranked between 200 and 300 on the ASX the median level of profitability has increased from $12 million to $31.77 million and the average from $11.37 million to $29.47 million.

The tables below highlight the average profit before tax across the ASX 300 which varies from $339.9 million to $513,01 million. On an industry basis the following table provides a report on results and each of the three calendar years together with the median values.

There is clearly variability across industries with the average level of profitability in the financial sector being a negative 7% between the 2015 and 2016 Financial Years and a 6% uplift in the 2017 Financial Year. The materials sector revealed the most dramatic change with the increase in the first Financial Year being a negative 72% and then 1,200% in the 2017 Financial Year. This reveals a significant impact of changes in commodity prices and export activity.

In telecommunications there was a significant negative outcome in profitability in the most recent Financial Year. In real estate it was positive in both years, being 28% uplift in the first and 17% in the second.

In consumer staples there was a 50% decline in the first financial period though a 94% improvement in the second. In utilities there was a negative 70% followed by a 360% uplift. Health care was relatively neutral with a 7% improvement in the 2016 Financial Year followed by a negative 7% in the 2017 Financial Year.

Industrials demonstrated a 37% adjustment on average in the first Financial Year followed by 25% in the second. The energy sector reflected a continuous negative impact with consumer discretionary revealing an average adjustment of 330% in the first period followed by a 24% adjustment in the 2017 Financial Year with the information technology sector revealing a 34% increase in the 2016 Financial Year followed by a 13% increase in the 2017 Financial Year.

The histograms below reveal the industry variability and the tables above the average movement in earnings by industry sector in the ASX 300. It reveals across the entire ASX 300 there was a marginal decline between the 2015 and 2016 Financial Years though a significant uplift between the 2016 and 2017 Financial Years.

Future Profit for Sharing

Given market sentiment is that the 2018 Financial Year will reveal an indicative uplift in the range of 5% to 7%, this reveals an average improvement across each ASX300 organisation in the range of $25.65 million and approximately $36 million.

If between 20% and 30% of the average profit uplift were allocated for profit sharing and assuming a middle of the road outcome in relation to forecast, there would indicatively be between $6 million and $9 million available for distribution to employees.

If the average employee population that is currently exempt from participation in a bonus or incentive plan across all enterprises, whose employee numbers would vary from in excess of 100,000 to less than 500, were 4,000 then indicatively there would be $1,875 per employee through profit sharing, or $36 per week which would represent a significant uplift to the minimum wage earner and leave approximately 30% of after tax profit improvement to be retained for further investment and 25% to be distributed to shareholders.

This macro market assessment is obviously not one which will be universally available in all sectors. As will be observed above, some sectors are challenged. The data also reveals variability of profitability in each of the last three Financial Years, as reported, up until 31 December 2017. Sectors which employ very large numbers of employees would include those in both consumer staples and consumer discretionary sectors. They are clearly not the most profitable sectors in the current environment where household expenditure is under pressure.

It is acknowledged that distribution of profits to the least well-paid employees can be managed on a pre-tax basis whereas retained reserves and distributions to shareholders will be on a post-tax basis. Given the current legislative environment and the lack of universal support for a reduction in corporate tax, recent portrayed experience enjoyed in the United States where there was a significant reduction in corporate tax compared to that foreshadowed over the next decade in Australia, the challenge of managing enhanced rewards for Australian employees will be a shared burden for enterprises and legislators with key points of influence in the period ahead being the sponsorship of innovation and the broader application of technology, the alignment of educational outputs with the changing world of work and a commitment of all stakeholders to encourage increased returns from employee input through building more direct rewards for that contribution.

While the above has drawn data on the ASX 300, the principle should have universal application. There is also an implication that senior management’s total reward, while not leading the world, have increased at a far greater rate than that of the average member of the nation’s workforce. With continuous profit improvement in the years ahead, tax reform and an adaptive workforce every stakeholder should benefit.

Conclusion

If a construct were to be introduced where the prior incentive pools were contained for distribution to current participants in annual incentive plans for one or two years, then in principle with government tax reform. targeted investment and transformation initiatives delivering improved profitability and the adoption of strategies for containing fixed costs the general workforce could benefit through gaining a new share of improved performance.

Adopting this approach may well require further attention by management in ensuring that profit is not distributed to an unproductive segment of their workforce while acknowledging the contribution made by the least well-paid employees in their enterprise.

The funding of this enhanced annual reward would be delivered through a profit-sharing construct and not a mandatory or imposed set of wage adjustments, whether delivered through a flow-on of increases to the minimum wage, the adherence to long-established penalty rates in an environment where days of the week are not acknowledged in the same way as they were two generations ago.

Policy makers, labour leaders and corporate leaders need to explore avenues for improving the welfare of all workers without encouraging a transfer of Australia’s investment into low cost economies which will not advantage Australia over the longer term.