The link between pay and performance for traditional long term incentive plans can be broken by certain scenarios in volatile markets.

Two such scenarios are where:

- Executives’ efforts lead to relative outperformance against a peer group or sector, but shareholder value reduces or remains flat.

- Executives receive significant payments due to outperformance that are worth many times the original remuneration intent of the Board.

Egan Associates believes further thought is required on the vesting conditions of securities under long term incentive plans to combat the effects of these scenarios and ensure reward and performance remain aligned in volatile markets. In this article, we outline our thoughts on the scenarios and underline our viewpoints via analysis of a hypothetical grant situation using ASX 100 performance.

Scenario 1: Relative Outperformance without Increasing Shareholder Value

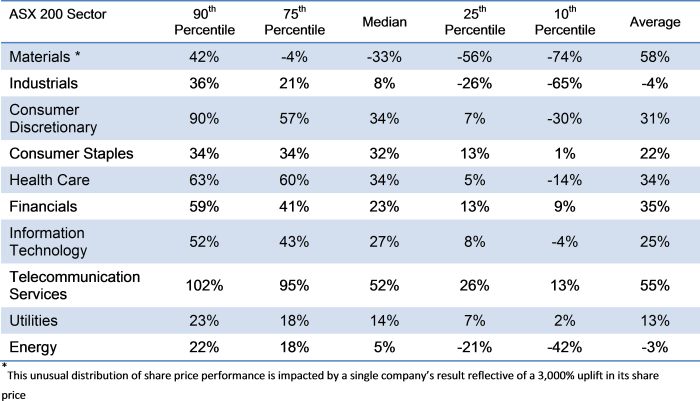

To illustrate this scenario, consider the share price movement among the ASX 200 for the financial year to 30 June 2013. The range of movement has been significant, with some sectors performing well, while others have performed poorly.

Taking the Materials sector as an example – given the 33% median sector share price fall, BHP’s flat share price performance means it outperformed the sector. Yet it has done poorly in comparison to the ASX 200 and ASX 100 index as a whole and has not delivered value to shareholders.

Herein lies the catch 22. Do we reward BHP’s executives for doing better than most of its sector or do we punish them for failing to foster shareholder value? Should performance payments reflect absolute improvement from the prior year(s) or relative outperformance which may not reward shareholders?

We have seen the ire of shareholders who have objected to bonus payouts when a company has been suffering under losses or poor performance or return to a modest profit after a year of losses. In some past cases, such as Bluescope Steel, this led to a strike on its remuneration report in 2011 (although we note that in this case there has been a significant recovery in the company’s performance in terms of share price in the 2013 Financial Year).

Awards vesting under long term incentive plans can be less obvious to shareholders, but does this mean shareholders would be pleased if they knew executives reaped rewards while shareholder returns remained meagre or negative in an absolute sense?

Considering these issues, Egan Associates would ask:

- Should all long term incentive plans have the requirement that there can be no vesting unless there has been positive share price improvement or Total Shareholder Return at least equal to the compound growth in the consumer price index (CPI) since the grant date?

- Alternatively, should there be a requirement that grants not vest if the current share price is lower than it was at the date of grant?

- Or should we take long term incentives back to fundamentals? This would mean judging performance no longer on the growth in shareholder wealth itself, but rather the base on which shareholder wealth is created, such as growth in earnings, growth in return on capital and/or growth in revenues.

Scenario 2: Excessive LTI payments for Significant Outperformance

Boards should not only consider whether outperformance in a declining market should lead to reward but also whether an extended bullish market for a particular sector should lead to management – who are generally less significant investors than shareholders – receiving rewards of many times greater than what is predicated under the company’s reward structure. This is often exacerbated by the practice of using accounting standards to allocate grants of equity: the prevailing share price is discounted to account for factors including dividend policy, the possibility that the company will not outperform the market and the award will not deliver a benefit.

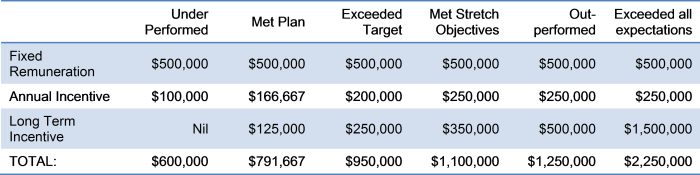

Portrayed below is a remuneration structure, which subject to certain performance outcomes, highlight this dilemma:

The remuneration intent of the above reward structure is that if the executive achieves superior performance, their variable remuneration (short and long term incentive) will total 100% of fixed remuneration. The tables below portray variable performance and reward outcomes.

From the table, it can be seen that no matter what performance the executive achieved, the maximum short term incentive received was $250,000, equal to the original remuneration intent. Although the company performed best in the two scenarios on the right (perhaps because of a bull market or cyclical sector conditions), the executive does not receive more than the stretch target award.

The value of the long term incentive award on the other hand, is not capped, rising in tandem with the company’s performance. In the “Exceeded all expectations” scenario, the long term incentive is worth 300% of the fixed remuneration award, or six times the stretch performance remuneration intent.

We note that many comprehensive annual incentive plans set the maximum award for significant outperformance at either one-and-a-half times or twice the target, leading us to ask:

- Should this principle also be applied to long term incentive awards, where the value of the award vesting to the executive would be capped at twice the value of the award as disclosed to shareholders, irrespective of the market’s performance?

- Where outperformance in an underperforming sector arises, should the benefit be capped at the threshold or, say, half the underlying award value?

Grant Analysis

We explored the likely return to executives in the ASX100 for a hypothetical $100,000 grant of shares and $100,000 grant of options, with vesting benchmarked to relative Total Shareholder Return for the ASX 100 over the most recent 3-year award period: awards following the 2009 Annual General Meeting and vesting in the final quarter of 2012. The vesting schedule saw 50% of shares or options vest at median Total Shareholder Return performance, while 100% vested at 75th percentile performance.

Total Shareholder Return was measured using 60-day smoothing. Unsmoothed share price adjusted for capital events was taken at grant date and vesting date. The number of options to be granted was calculated using the Black Scholes formula for an exercise price equal to strike price.

We note that the data we displayed in scenario one highlighted that using a broad index such as the ASX 100 to identify whether an executive team has performed may not reflect management accomplishments, but believe that it is adequate for us to illustrate our points.

The following highlights the movement in share price in the ASX100 in the three years from September 2009:

The table below sets out the value of vested shares and options over the same sample.

Due to the vesting schedule, no shares or options vested below the median. Yet despite a fall in median share price, there was vesting of shares at median, such that executives who presided over a fall in share price over the three years received a benefit from their long term incentive plan. This can be seen in the table below, showing the share price growth distribution for companies where at least part of executives’ rewards vested.

Just over 25% of participants whose shares vested received an award despite a fall in the share price over the three years. These executives would not have received any award if there were an additional condition that the share price be greater than that at the starting date. Of course, there was no reward under the option grant in this case. We would note, however, that the value of awards under the options plan were 50% higher on average than those under the share rights plan and that the best performers received well over the original remuneration intent for the options plan.

Approximately 40% of executives whose shares vested received an award even though the compound annual growth rate of the share price was less than 2% – the lower end of the RBA’s inflation target. The average award for these executives was just under $70,000. For the options the average award was only around $4,000.

We would note, however, that the performance of those executives where vesting occurred was significantly better than those where vesting did not, as can be seen in the distribution below.

We also note that the allocation of securities at grant date where the share price may be at an all time high or 20% of the share price at the time of the prior year’s grant can also skew rewards to be either high or low.

Conclusion

The area of what is reasonable remuneration requires continuous review. It is our judgement that these matters should be elevated to open debate at Board level. We have, over many years, brought these issues to the attention of our clients, both Executives and Directors. We do not think that organisations have yet landed on the ideal system.

We suggested in our last newsletter that the traditional long term incentive might be replaced by an elevated short term incentive where 50% is awarded in deferred shares. Not only would this help reduce the difference between remuneration intent and value to the executive and give management skin in the game from the outset, but as we mentioned, this has the added benefit of reducing complexity which may help with motivation. Executives understand how their contribution leads to incentive awards, as opposed to knowing they have a ticket in a lottery that may or may not pay out.