It is an often-held view in the general public, and indeed by many executives themselves, that they will not be struggling in retirement to meet their needs.

However, the reality for many executives not in the top tier of Australian companies is that they may find it difficult to maintain their quality of lifestyle over an extended period of retirement.

Indeed, it appears many executives are not even contributing to the full extent of their available superannuation concessional contribution cap.

The median amount of superannuation paid on behalf the top five executives excluding the CEO for companies ranked 100 to 600 by market capitalisation (at 31 March 2015) in the 2014 financial year was approximately equal to that required for the maximum superannuation contributions base (circa $18,000).

CEOs appeared less sanguine about their retirement. The median superannuation for CEOs was approximately $25,000, which was the concessional contributions cap for the 2013-2014 year for those aged under 59. The $25,000 contribution was reached by the 75th percentile of executives excluding the CEO.

Individuals over 59 at 30 June 2013 could contribute $35,000 (the age reduced to 49 years on 30 June 2014). Only the 90th percentile of CEOs had this much superannuation recorded as part of their remuneration, with the 90th percentile of top 5 executives contributing approximately $30,000.

The question arises, is salary sacrificing to the concessional cap onerous for these executives?

To answer this, we examine their accessible annual income for the 2014 year (fixed remuneration and bonus paid in cash rather than deferred in shares). The median CEO of a company ranked 100 to 600 received approximately $670,000 at the median, while the other executives received approximately $400,000. If only considering companies ranked 300 to 600, this reduces to $540,000 and $330,000 respectively.

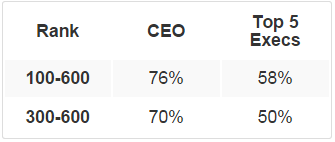

If superannuation contributions are limited to the value corresponding to the maximum contribution base, the CEO and top 5 executives retain most of their gross accessible income and after tax is paid they can spend it. Approximate amounts retained as a percentage are shown in the table below:

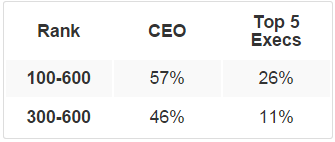

This was reduced if executives elected to sacrifice salary up to the 2013-2014 concessional cap of $25,000:

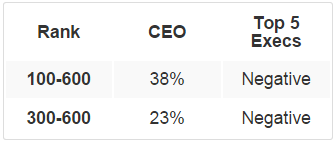

If sacrificing to the 2014-2015 salary cap of $35,000, assuming executives are over 49, this reduces to:

Contributing above the level of concessional contributions becomes more difficult, with a greater effect on accessible income. Given this is the same or less than the 9.5% current superannuation rate most Australians must contribute to superannuation, the question must be raised as to why a larger proportion of executives are not doing so.

If the executives contributed non-concessional contributions in addition to concessional, because the contributions are post tax, a larger amount of an executives’ pay packet is sacrificed.

Assuming:

- The executive wanted to contribute a) $50,000 b) $100,000 or c) $150,000 in non-concessional contributions (one third, two thirds or all of the 2013-2014 non concessional cap) in addition to a $25,000 concessional contribution for 2013-2014, and

- The executive is paying tax at the rate of 47% (excluding the temporary debt levy but including the Medicare surcharge and disregarding any deductions)

the percent of gross accessible income retained would be:

a) For a $50,000 non-concessional contribution:

b) For a $100,000 non-concessional contribution:

c) For a $150,000 non-concessional contribution:

If this were increased to 2015-2016 limits, assuming executives were over 49 and contribute to a concessional cap of $35,000 and a non-concessional cap of $180,000, the gross amount retained would be:

a) For a non-concessional contribution of $60,000:

b) For a non-concessional contribution of $120,000:

c) For a non-concessional contribution of $180,000:

As the above reveals, it is not easy or indeed possible for every one of these executives to contribute superannuation to the maximum amount they are entitled per year on a regular basis.

The question then becomes, do executives need to contribute at this amount to achieve a superannuation balance that will enable them to be comfortable in retirement?

Let us investigate how much these CEOs and executives would have in their superannuation when they retired if they contributed at:

- The maximum contribution base.

- The limits of the concessional cap.

- The limits of the concessional cap and one third of the non-concessional cap.

- The limits of the concessional cap and two thirds of the non-concessional cap.

- The limits of the concessional cap and 100% of the non-concessional cap.

Assumptions:

- The CEOs/executives are 50 in the 2015-2016 year.

- They currently have $500,000 in their super (as a conservative estimate considering the 90th percentile of annualised weekly wages for earners of that age is around $128,000 according to Australian Bureau of Statistics data, and the 90th percentile of superannuation balances falls around the $200,000 to $299,000 range for that age according to the Association of Superannuation Funds of Australia statistics).

- The concessional contribution is taxed at 30% upon accumulation, even though executives who are close to the $300,000 barrier and are carefully managing their tax affairs may utilise tax deductions to reduce their taxable income and may not be eligible for the additional tax.

- The maximum super contributions base increases by 4% a year (based on an average of the increases over the last ten years). The super guarantee rate increases as planned to 12% in increments over the period from 2021-2022 to 2025-2026.

- The concessional contributions cap is indexed at AWOTE rounded down to the nearest $5,000 (the $35,000 is a temporary cap limit, which will be superseded once the index contributions cap passes it). The CAGR for full time adult AWOTE over the last ten years has also been around 4%.

- The non-concessional cap is a multiple of the concessional contributions cap.

The approximate superannuation balance at retirement given net returns on the portfolio of 3%, 6% and the APRA-provided five-year average annualised return of Australian super funds of 8% are:

Where contributions are made at:

- The maximum contribution base.

- The limits of the concessional cap.

- The limits of the concessional cap and one third of the non-concessional cap.

- The limits of the concessional cap and two thirds of the non-concessional cap.

- The limits of the concessional cap and 100% of the non-concessional cap.

The analysis shows that these executives could have between $870,000 and $10m in their superannuation by the time they retire.

While the executives are likely to also own their home, the Productivity Commission noted in its recent Superannuation Policy for Post Retirement report that Australians do not usually tap the wealth in their home to provide income in retirement, instead using it as a safety net for potential costs later in life such as aged care.

According to the same report, a woman who is currently 65 can expect to live another 31 years in retirement and a man between two to three years less.

Research on safe withdrawal limits in retirement by Financial Services Institute of Australasia, a membership association for financial services professionals, shows that if individuals want their funds (invested 50% in growth assets and 50% in defensive assets) to last for thirty years with only a 10% chance of running out, the maximum annual withdrawal rate based on historical data is 3.62%.

Disregarding the minimum withdrawal rate for superannuation (as the executive could potentially withdraw at higher levels and reinvest outside the tax-exempt environment if required) and using a 3.62% withdrawal rate as an indication, executives would have initial income levels that were approximately:

These would fluctuate up or down with time depending on market returns.

All of the annual income amounts are above the level of the full single pension and ASFA assessment of modest retirement lifestyle expenses for singles. A balance of approximately $1.2 million or above is required to match the ASFA comfortable retirement lifestyle expenses for singles.

For those hoping to maintain their current lifestyle, a common yardstick is two thirds of current income, but amassing the necessary wealth in superannuation appears to be out of reach, for top paid executives because that would require them to contribute beyond the bounds of their income, and for CEOs because they would breach contribution limits.

However, it is clear that those who do contribute additional amounts can maintain respectable incomes in retirement, even if international travel is taken into account.

What if the market is performing badly?

The 3.62% rate is based on the past performance of Australian investments, which may be misleading, as the Australian market has performed particularly strongly over the last century, a trend some experts believe unlikely to continue. Finsia examined 17 developed countries in its analysis, and found the maximum withdrawal rate was over 4% for four countries, between 2% and 4% for eight countries and under 2% for five countries.

If the executive wanted to be sure their portfolio would not fail, they could adjust withdrawal rates based on market returns, which could lead to commensurately lower income levels.

Conclusion

Executives should be aware of their expectations in retirement and the amounts they are contributing to superannuation. If the latter will not achieve the former, executives should consider increasing their contributions within the limits to which they can contribute under the current regime.

Given the amount of debate around superannuation concessions, the rules may not remain static over the next few years. There have been a number of submissions to the Federal Government’s taxation whitepaper suggesting changes that will affect the ability of individuals to use the government’s tax concessions to help save for retirement. Executives must keep the potential for changes in mind when making any decisions.

Some of the suggestions in submissions to the review include:

- Limiting tax exempt balances to $2.5 million – as shown, this can affect executives who contribute above concessional caps.

- Reducing the threshold for 30% tax on super accumulation to those with incomes over $180,000. It is currently set at $300,000. This would affect executives who have structured their tax affairs to avoid the additional taxation.

- Implementing a flat tax of 12% for superannuation accumulation, earnings and withdrawals. This will affect assumptions around the tax-exempt status of super during the drawdown phase.

- Increasing the age at which individuals can access superannuation to 65. This could affect the plans of those who are hoping to retire early.

Other possible scenarios for inclusion in superannuation scenario planning for the next 50 years could include:

- Limiting lump sum withdrawals from concessional superannuation fund accumulation to 10% of the fund balance at retirement age.

- Requiring high income earners to make mandatory contributions at concessional rates up to the superannuation guarantee percentage of their annual cash income, capped at $100,000 per annum.

- Reducing the current mandatory aged-based superannuation withdrawal rates, with current rates to be considered as maximum withdrawal rates.